Welcome to the Financial Times:

"Our best content for legal services"

Below you’ll find a handpicked selection of our award-winning journalism pieces, showcasing a range of topical news articles,

popular features as well as premium commentary and analysis.

The FT brings a unique global perspective to news coverage, from the fallout after the EU referendum and a snap election

to the Trump presidency, our network of correspondents provide detailed reporting and essential analysis of major

events and trends in a changing world.

A big red bus emblazoned with the words “we send the EU £350m a week, let’s fund our NHS instead” is credited as being decisive

in Britain’s vote to leave the EU last year.

It promised — in absolute terms — financial gains for the British public if they voted to leave, a stark counterweight to

a majority of economists who warned that a departure would hurt Britain. The pre-referendum estimates of

the long-term pain ranged from a hit to the economy of 1 per cent to 9 per cent of national income — an annual

loss of gross domestic product of between £20bn and £180bn compared with remaining in the EU.

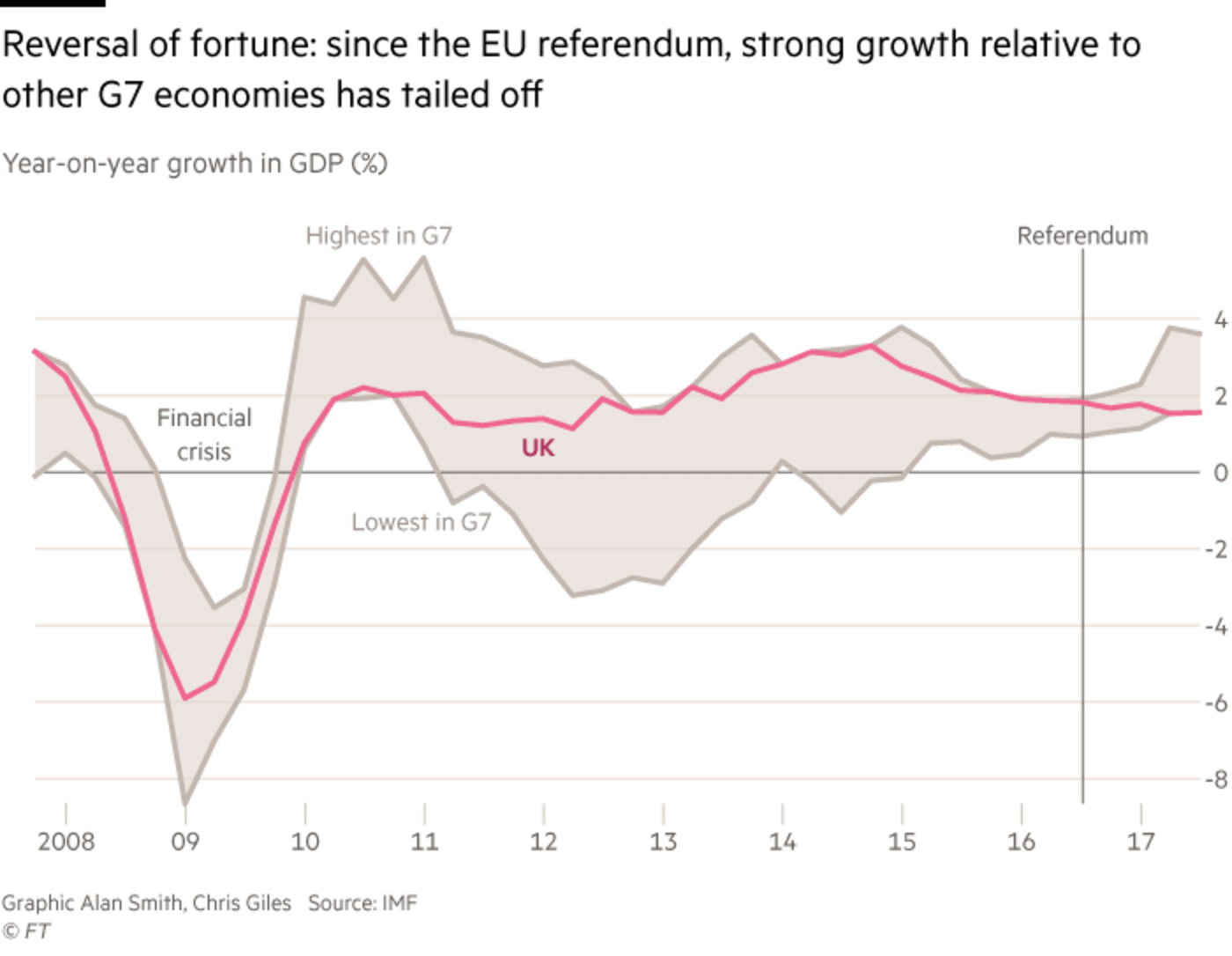

The Leave campaign won the battle of the slogans, and the referendum. But who is winning the economic argument? Almost 18

months on from the Brexit vote and with 15 months of detailed UK data, it is now possible to begin to answer

that important question.

Economists for Brexit, a forecasting group, predicted that after a leave vote growth in GDP would expand 2.7 per cent in

2017. The Treasury expected a mild recession. Neither proved correct. The 2017 growth rate appears likely

to slow to 1.5 per cent at a time when the global economy is strengthening.

According to economists such as Robert Chote, chairman of the independent Office for Budget Responsibility, which produces

the official government forecasts, a more pressing question is to assess the impact compared with what would

have happened had the vote gone the other way. “Many PhDs are going to be written on the impact of Brexit

over the years to come,” he says.

This work has started, and includes a range of estimates calculated by the Financial Times suggesting that the value of Britain’s

output is now around 0.9 per cent lower than was possible if the country had voted to stay in the EU. That

equates to almost exactly £350m a week lost to the British economy — an irony that will not be lost on those

who may have backed Leave because of the claim made on the side of the bus.

Jonathan Portes, professor of economics and public policy at King’s College London and one of the academics leading publicly

funded research into the effects of Brexit, says: “The conclusion that, very roughly, Brexit has already

reduced UK growth by 1 per cent or slightly less seems clear.”

Companies are becoming more vocal over the economic hit, blaming the government’s slow handling of the Brexit negotiations

for a weaker business climate. In October, the International Monetary Fund highlighted Britain as a “notable

exception” to an improving global economic outlook, while the OECD, the Paris-based club of mostly rich nations,

has raised concerns about “the ongoing slowdown in the economy induced by Brexit”.

Thomas Sampson and colleagues at the London School of Economics have examined the direct effect of sterling’s depreciation

since the EU referendum on prices and living standards. With the pound falling about 10 per cent following

the June 2016 result, inflation has risen more in Britain than in other advanced economies. It started with

petrol prices and spread to food and other goods, pushing overall inflation up from 0.4 per cent at the time

of the referendum to 3.1 per cent last month.

When looking at prices, depending on the level of import exposure of different goods and services, the LSE study estimates

that the Brexit vote directly increased inflation by 1.7 percentage points of the 2.7 percentage-point rise

in the 12 months after the referendum. And with wage inflation stuck at just over 2 per cent, “the increase

in inflation caused by the Leave vote has already hurt UK households”, Mr Sampson says.

He calculates that “the Brexit vote has cost the average worker almost one week’s wages”, but adds the figure could be higher

or lower if a complete evaluation of the economic impact was applied rather than just the initial squeeze

on incomes from leaving the EU.

Other effects are more apparent. Business investment grew at an annual rate of 1.3 per cent in the third quarter, compared

with a March 2016 official forecast for annual growth of 6.1 per cent for the whole of 2017. Exports, boosted

by sterling’s depreciation, have proved more resilient. The OBR now expects a 5.2 per cent rise in the volume

of goods and services sold abroad in 2017 compared with a pre-referendum prediction of 2.7 per cent.

Net migration to the UK from the EU fell by 40 per cent in the first 12 months after the vote. Professor Portes last year

predicted an ultimate decline of between 50 and 85 per cent on net migration levels before the referendum.

“Arithmetically, this reduction [of 40 per cent] of net EU migration translates into a reduction in growth

of 0.1 to 0.2 per cent,” he says.

Economists working to estimate the overall Brexit impact on the economy need to build a counterfactual scenario — an imagined

world in which Britain had voted to remain in the EU — to compare that with Britain’s economic performance

since the vote. The counterfactual cannot be known for certain but it is possible to take a number of approaches,

in three broad categories.

The first is to compare recent UK economic performance with its past. A worse performance than the UK has achieved over long

historical periods or in recent years would support the view that the vote has hurt economic performance.

But a shortcoming of this approach is that if the past year was always likely to be rather weak, this method

could suggest a Brexit hit when there was none.

Comparing the UK performance with that of other countries is another option. Using its normal position in the G7 league table

of leading economies is one possible technique, as is contrasting UK performance with the average of similar

economies. A more sophisticated approach is to use a statistical algorithm to devise a historically accurate

set of comparator countries, a method recently performed by a group of academics from the universities of

Bonn, Tübingen and Oxford. These geographical techniques often smooth out concerns that the recent period

might be unusual, but they are vulnerable to variations in other countries, such as a sudden boom in the

eurozone that Britain was never likely to match.

A third tactic is to look at forecasts made for Britain’s economy before the referendum on the basis of staying in the EU

and compare the actual outcome with these prior forecasts. Its weakness is that there was a wide range of

pre-referendum forecasts, while its strength is that the figures reflect the best knowledge available at

the time.

Net migration to the UK from the EU fell by 40 per cent in the first 12 months after the Brexit vote.

Jagjit Chadha, director of the National Institute of Economic and Social Research, says each of the methods are reasonable

for generating an estimate of the impact of Brexit so far. “We can’t know how the [UK] economy would have

responded to the news over the past 18 months, but there have not been any large shocks and the rest of the

world has done slightly better than we thought likely a year ago.”

The results vary according to the comparisons made, but all show the UK economy has been damaged even before it formally

leaves the EU on March 29 2019.

When the past five quarters are judged against the UK’s historical average growth rate, the 1.9 per cent expansion in GDP

achieved between the second quarter of 2016 and the third quarter of 2017 is lower than history would suggest

is normal for the UK economy.

Depending on the period of comparison chosen, the UK economy would normally have been expected to expand by between 2.5 per

cent and 3.2 per cent over the same period. The lower end of the range comes from more recent history, such

as the average since a Conservative-led government came to office in 2010, while the upper boundary reflects

Britain’s long-term performance in the 30 years before the financial crisis. The hit to the economy on this

comparison is between 0.6 per cent and 1.2 per cent of national income.

Geographical comparisons produce a similar conclusion. Britain’s year-on-year growth rate tended to be close to the G7 upper

range of outcomes over the past 25 years. Had that performance continued, British GDP would have grown 2.9

per cent since the referendum. The statistical algorithm produces a significantly larger estimate of what

would have been possible, suggesting Brexit has already removed 1.3 per cent from GDP since the vote.

This equates British performance to a weighted average of other countries, with the US, Canada, Japan and Hungary having

the largest weights. Asked whether it was reasonable to judge the UK’s performance against that of Hungary,

Professor Moritz Schularick of Bonn University says, “like the UK, Hungary is a European economy and integrated

into the production chains, but remained outside the eurozone with a floating exchange rate and therefore

could use monetary policy more aggressively after the crisis”.

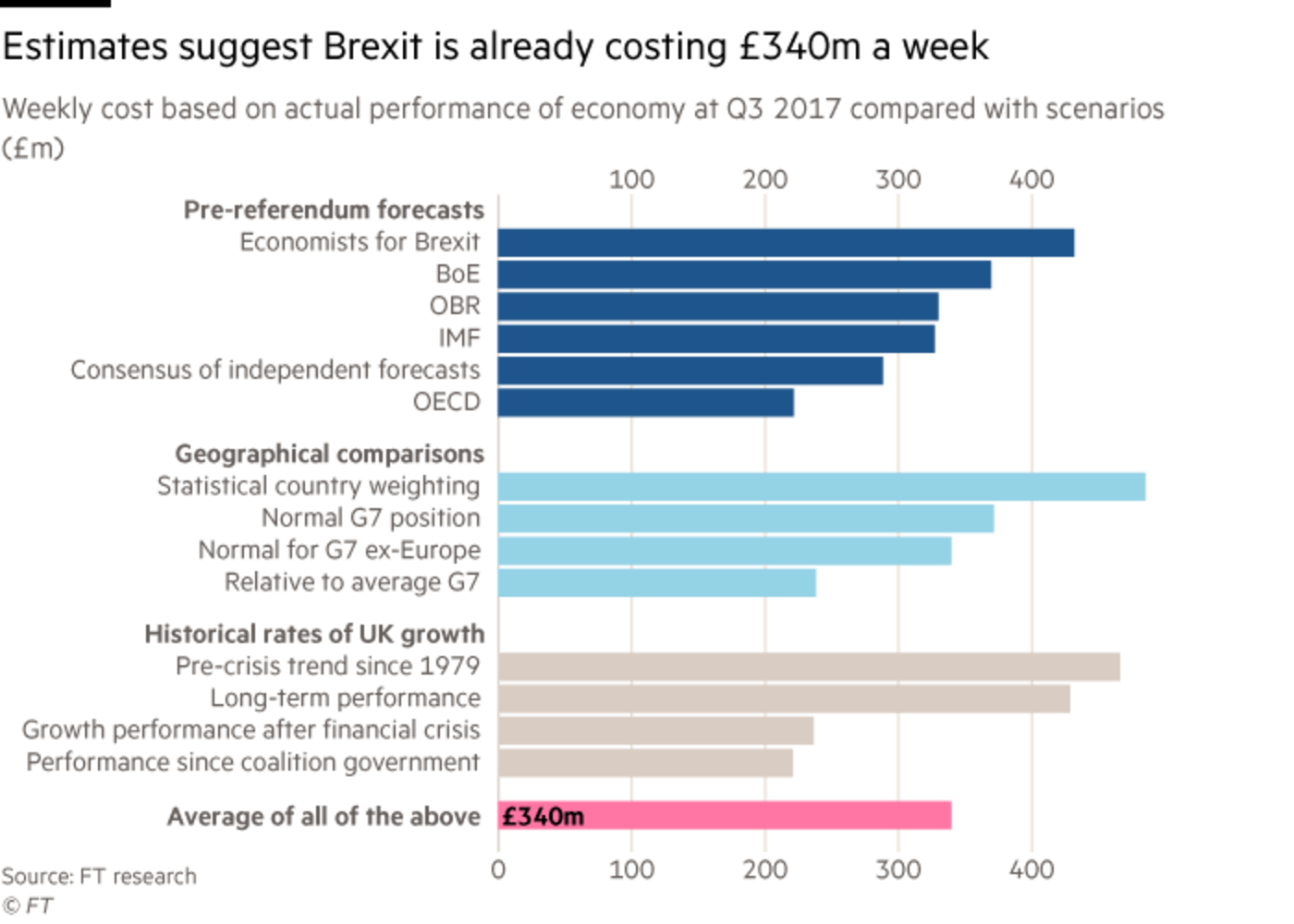

Estimates using pre-referendum forecasts provide a range within almost the exact same boundaries — between 0.6 per cent of

GDP and 1.1 per cent. The larger figure is based on analysis from Economists for Brexit, which initially

predicted strong growth after the vote.

Professor Patrick Minford, who carried out the forecasts for the group, blames “Office for National Statistics productivity

estimates, [which] are not convincing because they have made no real attempt to estimate the growth in quality

of services, such as in education and healthcare”. But all of this was known before the referendum.

Companies have been critical of Theresa May's government saying that delays in talks with the EU have hit

business

Overall, 14 different counterfactuals estimated by the FT and others give a range of a hit between 0.6 per cent of national

income and 1.3 per cent, with an average of 0.9 per cent. With national income of £2tn in the year ending

in the third quarter of 2017, it means the UK is likely to be producing £18bn less a year than would have

been reasonable to expect and this is directly attributable to Britain’s decision to leave the EU. That is

just short of £350m a week.

Brexit-supporting economists say the figures are reasonable. Julian Jessop, head of the Brexit unit at the Institute of Economic

Affairs, says: “Lots of sensible Brexiters accept there will be a short-term hit and it is unarguable that

the economy is weaker than it would have been, I would say between 0.5 and 1 per cent weaker. As for the

longer term, it’s all to play for. Brexit creates lots of opportunities, it is for the government to make

the most of them.”

In the referendum campaign the big red bus was making a different comparison, an incorrect one, about the budgetary costs

of the EU to Britain. It suggested Britain contributes almost £18bn a year to the budget, when the net cost

in 2016 was calculated by the Treasury to be £8.6bn. And this leaves one last comparison that it is possible

to make.

Paul Johnson, director of the Institute for Fiscal Studies, says that “for every 1 per cent of GDP you lose, that’s getting

on for £10bn a year of foregone tax revenues”. If 0.9 per cent of GDP has been lost over the five quarters

for which data exists, there has already been a £9bn hit to the public finances. So even before the UK has

left the EU, the referendum result is costing the UK government more than can possibly be recovered by ending

net contributions to Brussels.

Inflation has risen more in Britain than in other advanced economies since the Brexit vote rising from 0.4

per cent at the time of the referendum to 3.1 per cent in November

How the Brexit vote has hit the economy

0% - The average worker

After taking inflation into account, pay including bonuses for the average worker in October 2017 was £490 a week. Official

figures show that in May 2016 before the EU referendum it was £491, so real pay levels have been flat. This

squeeze on real incomes has constrained consumer spending growth and it has increased only because employment

has risen and household savings rates have fallen.

<11.5% - A company contemplating investment

Uncertainty over future trading relations with the EU has led companies to postpone some investment projects. Purchases of

lorries, vans and other transport equipment in the third quarter of 2017 were down 11.8 per cent on the same

period a year earlier, limiting the contribution investment made towards economic growth. The Bank of England’s

regional agents report that uncertainties over the UK’s trading ties“continued to deter investment for some

firms”.

>1.5% - A retailer facing a tougher trading environment

Sales in John Lewis, the department store favoured by Britain’s middle classes, have been 1.5 per cent higher in the second

half of 2017 than in2016. With inflation at 3.1 per cent, this implies a decrease in the volume of goods

purchased. To gauge what was possible at this most robust of UK retailers, the equivalent sales growth in

the second half of 2016 was 3 per cent, which at the time was well above the 1.2 per cent level of inflation

Hay Group uses the Financial Times to acquire and retain business clients worldwide"I use the FT to help me develop my thinking on business challenges my clients face…the FT often covers

issues or events that pertain to my key clients. I can either use these articles in a client conversation,

or they prompt me to drop an email or call a client, using the information in the article as a pretext

for contact"

85% of senior decision makers agree that the FT's coverage of the EU Referendum informs their business decisions**FT Reader Post Brexit survey

Empower your team or whole organisation to work better and smarter with an FT Group Subscription, or use an

FT Republishing Subscription to increase readership, engage clients, attract prospects and improve brand

awareness.

When Greenland left the European Community in the 1980s, the legacy rights of expatriate citizens were guaranteed with a

legal act of extraordinary simplicity: the operative article runs to just 85 words.

The fate of 4m EU and British expatriates looks far more uncertain and complex. One senior Brexit negotiator fears talks

on citizen rights could sink into “a horrible legal morass”.

“It’s immense. Every time you think you’re across it, you turn another corner and find another mess,” said another senior

EU diplomat.

Both London and the EU-27 agree on a broad goal: a reciprocal deal to guarantee the rights of 3m EU citizens in Britain,

and about 1m British expats within the union. But within the detail of that superficial agreement lies an

expat lifetime’s worth of politically sensitive choices.

Residence definitions, pension rights, unborn children, the ability to move, claim benefits, marry, divorce, even commit

crime and avoid deportation — an entire cycle of modern life is potentially touched by the Brexit agreement.

“We can’t hide the fact that it is complex,” said Guy Verhofstadt, the European Parliament’s chief Brexit negotiator.

“But if we base ourselves on the principles of reciprocity and a uniform approach by the EU-27 then in my view there is no

reason why we cannot find a lasting and equitable solution.”

Here the Financial Times runs through seven obstacles to a deal.

Nothing can be taken for granted

There is no systematic register of when expats arrived in their current place of residence. Worse still, EU officials think

it is not feasible to create a comprehensive one before the expected Brexit date in 2019. So even if some

rights are guaranteed, citizens will need to prove eligibility. Britain’s 85-page residency form offers an

insight on the bureaucracy ahead.

Not all expats are the same

No British politician has questioned the right to remain of legitimate EU migrants. But that is only one small sliver of

EU citizen rights. At issue are work rights, welfare access, health provision, discounted student fees, even

the ability to draw a UK state pension 50 years from now. And these rights depend on circumstances.

Under EU law, migrant workers have different rights to students, pensioners or jobseekers. Residing in a country for more

than five years — and thereby gaining “permanent residence” — is an important threshold for gaining rights.

But decisions will depend on proof.

Circumstances change

Managing change will be hard. If an expat marries, what rights would their partner enjoy, and would their nationality matter?

Could they bring in-laws to the country? Similarly an expat’s legal status may evolve over time, should they

lose their job or move country.

The law, too, will evolve. The EU may legislate to change rights post-Brexit. EU nationals may want to challenge Britain’s

application of their rights. Would that be in British courts or European courts? And whose interpretation

of EU law would prevail? A big role for European courts would cross a red line for London.

The two sides want to guarantee different rights

The EU-27 want to maintain full rights for EU expats but this could be tricky for Theresa May, the prime minister. If existing

welfare rights remain intact, for instance, EU migrants could still claim UK child benefit for dependants

in Paris or Warsaw — long a British tabloid bugbear. Full EU rights would also restrict Britain’s ability

to deport an EU migrant who has committed crimes after Brexit.

A third example is pensions. At present a Brit moving to Australia can draw their UK state pension, but it would be frozen,

and not increased in line with inflation and earnings. A Slovak or German migrant worker who leaves Britain,

by contrast, would enjoy better rights: their full UK pension drawn overseas and uprated every year.

There may need to be dozens of deals

Brexit poses two questions on citizen rights: the legacy rights of current expats and what terms future expats may enjoy.

Britain may seek to tackle both in one deal — reciprocated by the EU. That would apply a single, probably less generous,

regime of rights to all present and future EU migrants, covering health, benefits and citizenship.

Potential problems will arise from watering down EU rights. That is because the EU-27’s first and foremost concern is preserving

full rights for the existing 3m migrants, rather than future flows.

Depart too much from the EU’s legal baseline and EU negotiators warn a citizen rights deal may not be possible under the

Article 50 exit clause. Instead country-by-country bilateral deals may be necessary with each of the 27 members.

That is hard to negotiate and ratify, and even harder for expats to understand and apply.

Beware the cut-off point

No Brexit deal on rights can be open-ended. Negotiators are looking at various cut-off points: the lifetime of the eligible

expats; a period of time, say five or 10 years; or until the point at which the expat gives up their enhanced

rights by moving country. All three options have political and technical upsides and downsides.

One complication is that some rights, such as pensions, will be for life and even cover former expats. Then there is the

eligibility date. British ministers want to draw a line on EU free movement rights and are looking at three

options: the point of the Brexit referendum, the Article 50 notification, or Britain’s exit. EU-27 negotiators

see nothing to discuss: EU rights and obligations continue until the point Britain leaves.

Early, late or hard?

Expat rights will be one of the first topics to be discussed in Brexit talks. Both sides want a quick deal but that may be

impossible. Diplomats are scrambling to work out what would happen in the event of no deal. Expats would

basically be at the mercy of national governments.

But there are some protections. EU law does cover safeguard rights for some third-country nationals. And a raft of dormant

UK bilateral agreements with European countries on welfare — superseded by EU membership — may be revived.

One such agreement dug up: a 1923 Anglo-Finnish treaty on “the disposal of the estates of deceased seamen”.

Data protection

Between GDPR and ePrivacy regulation coming in 2018, and the constant risk of cyber attacks, the FT provides a trusted and reliable source for any changes and regulations implementation around data protection in the coming year.

The world’s biggest companies will spend tens of millions of dollars to meet new EU data protection laws by next May’s deadline, according to a survey that shows the costs of meeting some of the world’s toughest privacy rules.

Members of the Fortune 500 will spend a combined $7.8bn to avoid falling foul of Brussels’ General Data Protection Regulation (GDPR), according to estimates compiled by the International Association of Privacy Professionals (IAPP) and EY. This equates to an average spend of almost $16m each.

Among the biggest changes being ushered in by the GDPR is the right of individual citizens to request that their data be deleted from a company’s servers. It will also impose strict timelines on businesses to identify and report security breaches. Businesses face severe financial penalties for breaking the new rules: maximum fines will amount to €20m or 4 per cent of a company’s global annual turnover, whichever is largest.

Any business that processes the personal information of European citizens will have to comply with the GDPR.

The EU is already taking a tough stance on personal privacy. Tech giants such as Facebook are facing legal battles in European courts to ensure that they can legally transfer the personal information of their European users to and from the bloc.

Trevor Hughes, president of the IAPP, said companies had been rushing to hire lawyers and data protection consultants, invest in advanced data-processing software and clean up their sprawling databases.

“This is a rolling cost. May 2018 is by no means the end point as companies will have to invest in educating their employees in the new data framework,” said Mr Hughes.

On average, companies in the Fortune 500 will hire five full-time dedicated privacy employees — such as data protection officers — as well as another five employees to deal partially in handling the compliance rules, according to the survey.

“Data are emerging as the antitrust of the digital economy in the same way that state aid and competition was used to bust trusts in the 1990s,” said Mr Hughes. “This time, data protection has a direct consequence for consumers and citizens who use the digital economy.”

Financial services companies and the tech sector face the biggest compliance bills, according to the survey, which also estimates that medium-sized firms will spend an average of $550,000 to ensure they are compliant on May 28 2018.

Software companies are among the beneficiaries of the EU’s shake-up, which will change the way businesses have to handle, store and process personal data. Microsoft is among those helping companies who use their IT and cloud-based systems to ensure they comply with the GDPR. The company has at least 300 engineers dedicated to making Microsoft products compliant with the EU rules.

“We expect that the cost of our complying with the GDPR at scale, especially for our cloud services, will be much lower than the costs our customers would need to spend to manage all of their compliance individually,” said a spokesman for Microsoft. “We look at GDPR compliance from a business opportunity rather than a cost point of view.”

Analysts worry that smaller businesses are unaware of the looming changes. “I don’t know of any business which is ready or have said they will be ready by May,” said Lorraine Mouat, a consultant at TCC, which advises small UK financial firms on regulation.

Google illegally gathered the personal data of millions of iPhone users in the UK, according to a collective lawsuit led by a former director of the consumer group Which?

Richard Lloyd, a veteran consumer rights campaigner, alleges the technology company bypassed the default privacy settings on Apple phones and succeeded in tracking the online behaviour of people using the Safari browser.

Google then allegedly used the data in its DoubleClick advertising business, which enables advertisers to target content according to a user’s browsing habits.

The lawsuit, filed in London’s High Court, alleges Google’s tactic, known as “the Safari Workaround”, breached the UK Data Protection Act by taking personal information without permission.

“In all my years speaking up for consumers, I’ve rarely seen such a massive abuse of trust where so many people have no way to seek redress on their own,” said Mr Lloyd, who has set up a group called Google You Owe Us.

Google said: “This is not new — we have defended similar cases before. We don’t believe it has any merit and we will contest it.”

Google has already paid millions of dollars to US states and the US Federal Trade Commission over the Safari security bypass.

The case is the first time such a collective action — where one person represents a group with a shared grievance, akin to a US-style class action — has been brought in Britain against a leading tech company over alleged misuse of data.

Roughly 5.4m people in Britain had an iPhone between June 2011 and February 2012 and could be eligible for compensation, according to the claim.

Mr Lloyd has secured £15.5m in backing from Therium, a company that funds litigation and has previously backed group claims such as the consumer action against Volkswagen in the scandal over diesel emissions.

The funds cover Mr Lloyd’s legal costs — he is being advised by the firm Mishcon de Reya — as well as insurance in case he loses and has to pay Google’s legal bills.

Although the size of any potential payout would be determined by the court, Mr Lloyd said he expected each claimant would receive several hundred pounds.

“We think there is a massive gap in the law in terms of consumer redress around data rights being breached,” he said. He hoped the battle would end up producing “a clear set of guidelines and precedent” for consumers as to how they could act collectively in similar cases.

Should Mr Lloyd win, those who can prove they were affected by the alleged data breach are likely to have several years to make a claim.

The case will be closely watched by consumer groups and data protection lawyers, with the control, use and security of personal information coming under increasing scrutiny.

In addition, new regulations coming into force across the EU next year include a provision for anyone whose data has been misused to instruct consumer protection groups to bring claims on their behalf.

Due Diligence is the must-read daily briefing on corporate finance, mergers & acquisitions, and private equity. From Tuesday to Friday at 5am UK time, we’ll send our curated briefing straight to your inbox. In it, you’ll find the most important stories, analysis, and insights from the FT and across the web curated by a team of specialist reporters from around the world. We also break news in the briefings that you can’t find elsewhere.

Due Diligence

Due Diligence

Due Diligence

Due Diligence Mergers & Acquisitions

Has WeWork fooled investors that it’s a tech company?

Welcome to Due Diligence, the FT’s daily deals briefing

What do you do when you are a company renting out office space that is being valued like a tech company? Party like crazy at a summer camp, obviously!

Adam Neumann, co-founder and chief executive of WeWork, and his employees had a great summer party this year to celebrate the phenomenal success of the start-up that provides office space to thousands of millennials across the globe.

Following the decision on Thursday by SoftBank and its Saudi-backed $93bn tech fund to invest $4.4bn in WeWork (read the FT story here), DD expects Neumann & co to party even harder next summer — maybe with Masayoshi Son, founder of the Japanese group, and the former vice-chairman of Goldman Sachs, Mark Schwartz, who will sit on WeWork’s board.

Yet why is SoftBank using its tech fund to back a company that doesn’t really seem like a tech company?

Maybe the answer is that WeWork is unlikely to be profitable in the near future, a defining feature of any respectable tech start-up. (WeWork is private so doesn't disclose its financials.)

Neumann said last year that WeWork, which currently has more than 160 locations in over 50 cities and 16 countries, expects to generate revenues of about $1bn in 2017. If that’s accurate it means that its current price-to-sales valuation is about 20 — a little lower than Snap’s P/S of 29 and a little higher than Facebook’s P/S of 15.

But when compared to Regus, a company that offers a similar service to WeWork’s that has nearly 3,000 locations in 1,000 cities and 100 countries, the valuation of SoftBank’s new investment seems to be somewhat out of whack.

London-listed Regus has a market capitalisation of about $3.5bn and sales nearing $3bn, giving it a P/S valuation of just over 1.

That’s a staggering difference. Maybe it's just a cool factor but that seems a stretch. Who knows if SoftBank’s Son will still be up to partying with Neumann in a few years when his company and tech fund will have to monetise their investment.

TMT

The FT covers a wide range of topics under Technology, Media and Telecoms. Our journalists are publishing the latest news and analysis on the ever-developing world of technology, from AI and Robotics evolution to the Tech Giants rise, as well as its impact on Aerospace, Personal technology, eCommerce and many more.

Pressure has been growing in the past few weeks for politicians and regulators to clamp down on the monopoly power of Big Tech. In a speech given in Washington DC on September 12, Maureen Ohlhausen, the acting chair of the Federal Trade Commission in the US, tried to pour cold water on the idea. “Given the clear consumer benefits of technology-driven innovation,” she said. “I am concerned about the push to adopt an approach that will disregard consumer benefits in the pursuit of other, perhaps even conflicting, goals."

Her words echo US antitrust policy of the past 40 years: if companies bring down prices for consumers, they can be as big and as powerful, economically and politically, as they want to be. This hugely favours companies such as Google, Facebook and Amazon, which offer up services and products, from search results to self-publishing platforms, that are not just cheap, but free.

Yet Ms Ohlhausen is overlooking a key point: free is not free when you consider that we are not paying for these services in dollars, but in data, including everything from our credit card numbers to shopping records, to political choices and medical histories. How valuable is that personal data?

It is a question of growing interest to everyone from economists to artists. For example, at Datenmarkt, an art installation cum grocery store set up in Hamburg in 2014, a can of fruit sold for five Facebook photos; a pack of toast for eight “likes” and so on.

The bottom line is that it is almost impossible to put an exact price on personal data, in part because people have widely varying behaviours and ideas about how likely they are to part with it, depending on how offers are posed. In one recent study, when consumers were asked straight out whether they would consent to being tracked by a brand name digital media firm in exchange for being targeted with more “useful” advertising, four-fifths said no. Yet another study published this year by researchers from Massachusetts Institute of Technology and Stanford University shows how pathetically little incentive is required to convince people to give up their entire email contact list. Students in the study were far more likely to do it if offered a free pizza.

One might argue that this is simply the market working as it should. Consumers were given a choice, and they made it. And whether or not it was a bad one is not for us to judge.

But as the latter study also showed, companies can nudge users to part with data more freely by telling them it will be protected by technology designed to “keep the prying eyes of everyone from governments to internet service providers . . . from seeing the content of messages”. In fact, the encryption technology in question could not guarantee this.

The bottom line is that big data tilts the playing field decisively in favour of the largest digital players themselves. They can extract information and plant suggestions there that will lead us to entirely different decisions, which results in ever more profit for them.

Not only is that too much power for any one company to have, it is anti-competitive and market-distorting in the sense that the basic rules of capitalism as we know it are being overturned. There is no equal access to market information in this scenario. There is certainly no price transparency.

The personal data we give away so freely are being lavishly monetised by the richest companies on the planet (Facebook’s second-quarter operating margin, for example, was 47.2 per cent). They get their raw material (our data) more or less for free, then charge retailers and advertisers for it, who then pass those costs on to us in one form or another — a dollar more for that glass of wine at the bistro you found via a search, say. They have a licence to print money, without many of the restrictions, in terms of all sorts of corporate liability, that other industries have to grapple with.

These companies are not so much innovators as “attention merchants”, to borrow a phrase from Columbia University law school professor Tim Wu. Economists have yet to put good figures on their net effect on productivity and gross domestic product growth. Surely it is high. Yet any tally would also have to include the competition costs as these firms devour competitors and reshape the 21st-century economy to suit themselves.

Whatever the FTC might say now, there are a growing number of legal cases that could change the ground rules for Big Tech. While American antitrust law has been based on very literal interpretations of the 1890 Sherman Act, lawmakers in Europe take a broader approach. They are trying to gauge how multiple players in the economic ecosystem are being affected by the digital giants.

I am beginning to wonder if we should not all have a more explicit right not only to control how our data are used, but to any economic value created from them. When wealth lives mainly in intellectual property, it is hard to imagine how else the maths will work. We are living in a brave new world, with an entirely new currency. It will require creative thinking — economically, legally and politically — to ensure it does not become a winner-takes-all society.

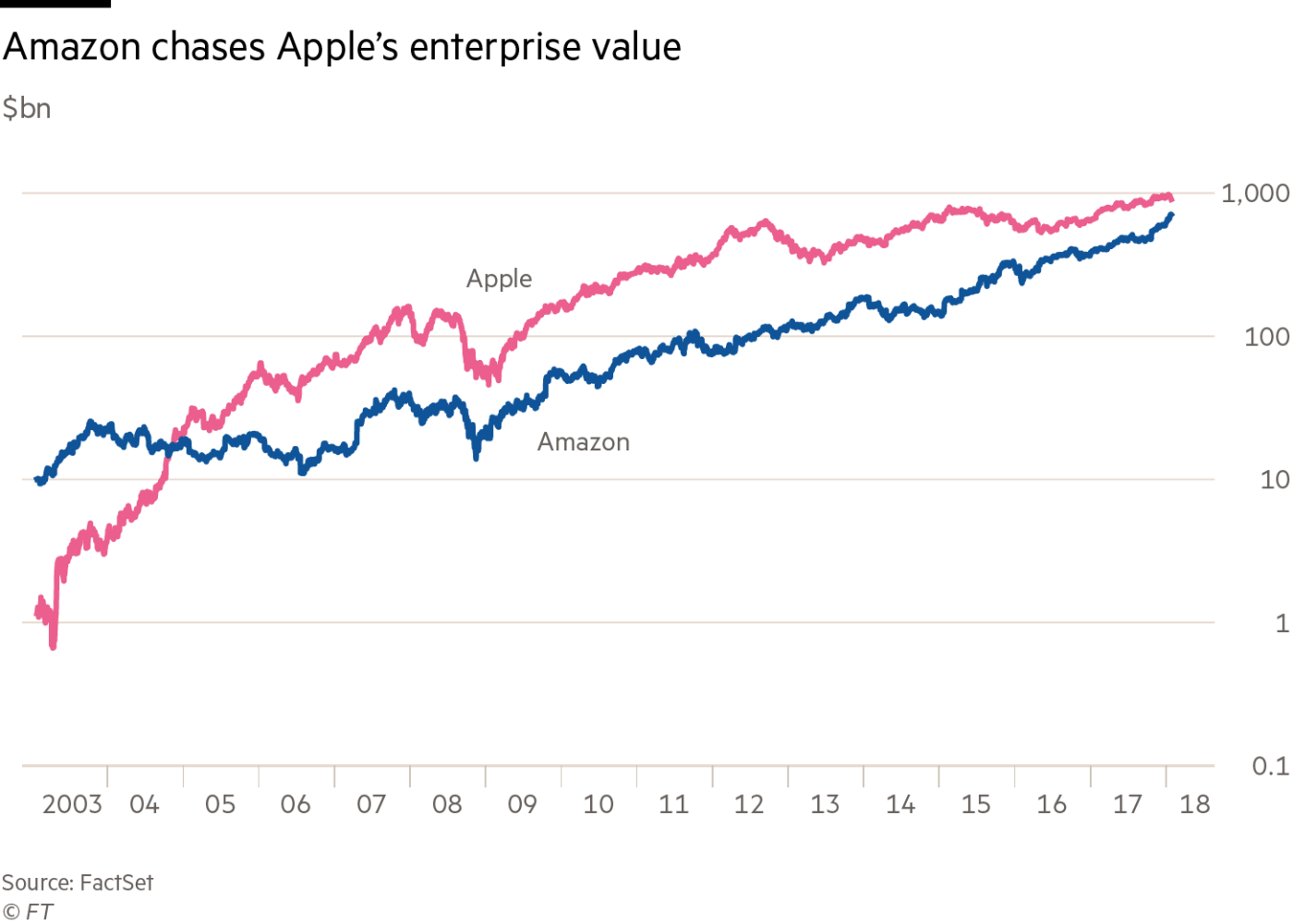

The Big Read Amazon

Big Tech and Amazon: too powerful to break up?

While Google, Facebook and Twitter are set for a grilling in Congress over Russia, it is the online retailer

that is drawing intense scrutiny

Amazon executives will not be present on Tuesday when three other major internet companies endure a grilling before Congress. But it may just be a matter of time before Washington’s new appetite for regulating the digital economy reaches the e-commerce giant.

Lawyers for Google, Facebook and Twitter will occupy this week’s spotlight in front of the Senate intelligence and judiciary committees, which are probing the companies’ unwitting role in Russia’s 2016 election meddling. Already, there is talk of legislation requiring them to disclose more about their operations.

The controversy over the industry’s dissemination of Russian “fake news” highlights a broader souring of attitudes toward the online platforms, triggered by unease over their sheer size and power, which spans the political spectrum. From progressives like Elizabeth Warren, Massachusetts senators, to Steve Bannon, President Donald Trump’s former chief strategist, who runs the nationalist media site Breitbart, there is growing support for reining in, or even breaking up, the digital groups that dominate the US economy.

“The worm has turned,” says Scott Galloway, a marketing professor at New York University and author of The Four: the Hidden DNA of Amazon, Apple, Facebook and Google. “No doubt about it.”

Though unaffected by the Russia allegations Amazon — whose $136bn in revenues last year topped the combined sales of Google parent Alphabet and Facebook — is a target of demands for more assertive antitrust enforcement. Its dominance has also raised questions about whether existing legislation needs to be rewritten for the internet age.

Jeff Bezos in 1999, introducing what became the Amazon marketplace

The online retailer’s relentless expansion into new businesses, including groceries and small business lending, and its control of data on the millions of third-party vendors that use its sales platform, warehouses and delivery services, have some analysts likening it to a 21st century version of the corporate trusts such as Standard Oil that throttled American competition a century ago.

“Amazon has big antitrust problems in its future,” says Scott Cleland, a technology policy official in the George HW Bush administration and president of Precursor, a research consultancy. “If there is a minimally interested, fair-minded antitrust effort in the Trump administration, Amazon’s got trouble.”

For now, Mr Cleland’s remains a minority view. Most experts say the company has yet to engage in the classic anti-competitive behaviour that the antitrust laws are designed to prevent. Under the prevailing interpretation of this doctrine, which prizes consumer welfare above all else, champion price-cutter Amazon has little reason to worry. Indeed, US regulators this summer performed only a brief review before approving Amazon’s nearly $14bn acquisition of the upmarket grocer Whole Foods.

Amazon and the other platforms remain popular with consumers, thanks to their low prices or “free” services. But companies that were once seen as avatars of American innovation and achievement are now increasingly treated with scepticism. Mr Bannon has said that companies such as Google and Facebook are so essential to daily life that they should be regulated as public utilities.

The digital platforms “dominate the economy and their respective markets like few businesses in the modern era”, says the bipartisan New Center project of Republican William Kristol and Democrat Bill Galston. It notes that nearly half of all e-commerce passes through Amazon while Facebook controls 77 per cent of mobile social traffic and Google has 81 per cent of the search engine market.

The online retailer stands alone in its cross-market reach, dominating product search, hardware and cloud computing while also serving as an indispensable conduit for other vendors to reach consumers, says Mr Galloway. Last year, 55 per cent of product searches began on Amazon, topping Google.

“They’re winning at everything,” he says. “This company is firing on all 12,000 cylinders.”

Yet even as calls to break up the nation’s big banks after the global financial crisis have faded, talk that the digital giants have grown too large gets ever louder. The downside of economic concentration features prominently in the Democratic party’s “Better Deal” programme for the 2018 Congressional elections. It calls for an intensification in antitrust enforcement and blames stagnant wages, rising prices and disappointing growth on insufficient competition.

An anti-monopoly push will “almost certainly” be a major part of the 2020 presidential campaign, predicts Barry Lynn of the Open Markets initiative.

Silicon Valley’s tradition of funding the party could complicate the Democrats’ anti-monopoly push. In the 2016 election, the internet industry gave 74 per cent of its $12.3m in congressional campaign contributions to Democrats. Internet company executives and their corporate political action committees, which pool individual contributions in accord with the federal prohibition on direct corporate political spending, also gave Hillary Clinton’s campaign more than $6.3m while Mr Trump pulled in less than $100,000, according to the Center for Responsive Politics.

Individuals and the PACs associated with Google parent Alphabet topped the industry’s list of total political contributors with $8.1m while Amazon ranked fourth with about $1.4m.

Amazon in numbers

Jeff Bezos in 1999, introducing what became the Amazon marketplace

542,000

The number of Amazon employees

17,000

The number of people who worked for the group in 2007

$2.4bn

Third-quarter revenues from subscription services including Amazon Prime

$1.4m

Amazon’s contribution to the 2016 US congressional campaigns. Overall the internet industry donated $12.2m — 74% went to Democrats

$13m

The amount Amazon is on track to spend on political lobbying this year. Up from $2.5m five years ago

Amazon has moved a long way from its roots since launching two decades ago to sell books and nothing but books. Now, it sells just about everything to everybody: nearly 400m products including its own batteries, shirts and baby wipes. It operates a media studio and provides cloud computing space to customers such as the Central Intelligence Agency while running the Marketplace sales platform for other vendors, a delivery and logistics network and a payment service. The company Jeff Bezos launched in 1994 also now makes popular electronics, including the Kindle ereader and the Alexa voice-activated device.

Its growth has been astronomical. Amazon expects to record at least $173bn in annual sales this year — that would nearly double its 2014 figure. It employs 542,000 workers, more than twice its mid-2016 payroll, thanks in part to the Whole Foods deal, and its $1,100 share price has roughly doubled in just 20 months.

By almost any measure, Amazon is a fantastically successful company. Maybe too successful, its detractors say. Mr Trump has periodically suggested antitrust action against the online giant, saying of Mr Bezos last year: “He’s got a huge antitrust problem because he’s controlling so much; Amazon is controlling so much.”

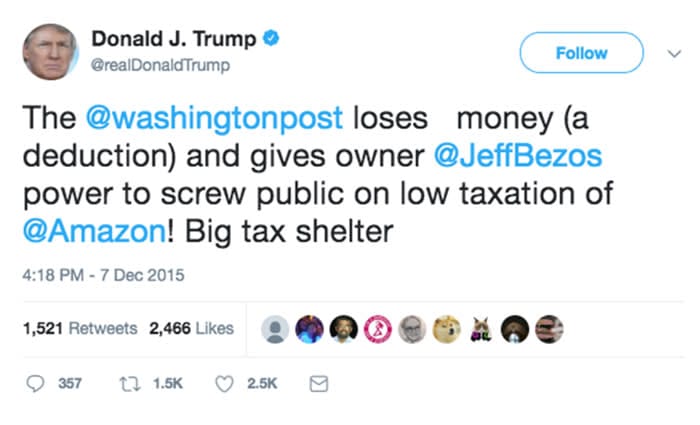

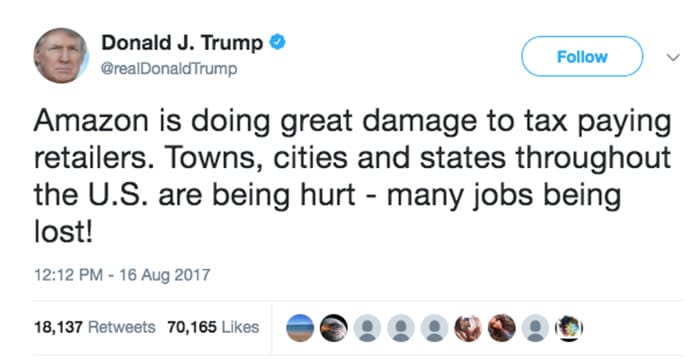

Donald Trump has frequently targeted the Washington Post, bought by Jeff Bezos in 2013. He called out Amazon on taxation in several 2015 tweetsDonald Trump continued his broadside against Amazon in an August 2017 tweet

In August, the president returned to the subject, taking aim at the company’s impact on bricks-and-mortar retailers. “Towns, cities and states throughout the US are being hurt — many jobs being lost!” he tweeted.

Still, most politicians regard Amazon as a potential economic boon. Some 238 communities answered the company’s request to identify sites for its planned second headquarters. It is not hard to see why: the $5bn project will directly create work for 50,000 people, plus “tens of thousands of additional jobs and tens of billions of dollars in additional investment in the surrounding community”, Amazon says.

Even critics of the company’s size, such as Senator Cory Booker of New Jersey, overcame their concerns. “Amazon would make the right business choice by coming here,” Mr Booker told a press conference last month in Newark.

Amazon, which declined to comment for this story, recognises its potential political problem. The company is on track to spend nearly $13m this year on lobbying the federal government compared with just $2.5m five years ago. In 2016 it added an antitrust lawyer, Seth Bloom, with experience on Capitol Hill and in the justice department.

Though the Trump administration approved the Whole Foods purchase, Amazon’s antitrust concerns have not evaporated. Congressman Keith Ellison, deputy chairman of the Democratic National Committee, who favours a break-up of all the digital players, says the online retailer should spin off its $12bn-a-year cloud computing business known as Amazon Web Services.

“I do think they should be forced to sell off huge parts,” he says. “They’re too big.”

The view is echoed by Mr Kristol, a prominent former official in the Reagan and George HW Bush administrations, who says the tech giants’ dominance hurts workers, consumers and the overall economy. His New Center project, aimed at overcoming political polarisation, supports tougher antitrust enforcement to address “monopolistic behaviour” in the technology sector.

Even among pro-market conservatives, sentiment is shifting on the need for greater government intervention. “People are at least open to the argument that concentration of power is a problem even if there’s no immediate cost paid by consumers,” Mr Kristol says.

US law does not prohibit monopolies so long as they arise through legitimate means. But companies are not permitted to exploit their dominance in one market to control another.

Competition authorities in the EU have moved more aggressively to corral the internet groups. Earlier this month the EU ordered Amazon to pay $290m in back taxes to Luxembourg after Margrethe Vestager, the EU competition chief, said the online retailer had benefited from special treatment.

Ms Vestager has also gone after American internet companies on antitrust grounds, levying a €2.4bn fine on Google in June and reaching a negotiated settlement with Amazon over its ebook distribution contracts. In May, Amazon agreed to scrap contract clauses requiring publishers to offer it terms that were as good or better than those offered to its competitors.

Amazon’s critics say that its role as an essential e-commerce platform for more than 2m other vendors and its control of data on their sales warrant government action. Last year, in a speech that ignited the Democrats’ renewed interest in anti-monopoly efforts, Ms Warren said companies like Amazon provide a platform “that lots of other companies depend on for survival”, adding, “the platform can become a tool to snuff out competition.” For its part, Amazon says it faces “intense competition”.

Critics remain unconvinced. Its control over a vast cache of customer data gives it “unprecedented . . . advantages in penetrating new industries and new markets”, according to Amir Konigsberg, chief executive and co-founder of Twiggle, which sells search and analytics software to Amazon competitors.

There’s no question that the company has grown through innovation and by meeting customer needs. But gobbling up rivals and would-be rivals has also been part of the equation. Since 2005, Amazon has acquired more than 60 companies including some that were at first reluctant to sell, such as Zappos, the online shoe retailer.

“It’s a dominant platform and a vertically integrated dominant platform,” says Lina Khan, author of an influential Yale Law Journal article earlier this year that ignited the debate. “It acts as a gatekeeper . . . It’s closing off the market to new entrants.”

Ms Khan says Amazon also has priced goods and services — such as its unlimited two-day Amazon Prime delivery service — below cost. By prioritising growth over profits, the company has unfairly squeezed competitors, she says.

Though Mr Cleland says antitrust enforcers could make a case against Amazon under the prevailing interpretation of US law, most analysts say a genuine push to break up or constrain the tech giants requires rethinking the antitrust orthodoxy of the past 40 years. The so-called Chicago School of antitrust theory, which focuses on consumer prices and innovation, is ill-equipped to cope with the internet world’s structural tendency to produce winner-takes-all outcomes.

“The rhetoric around consumer prices can disable antitrust law,” says Ms Khan. “These platforms present new issues.”

Antitrust: ‘Consumer first’ laws favour Amazon

It is almost four decades since Robert Bork, a one-time Supreme Court nominee, wrote the book that defines US competition policy to this day.

Mr Bork, a Yale University law professor, relied on Chicago school economics to argue in The Antitrust Paradox that safeguarding “consumer welfare,” not preventing excessive corporate size, should be the goal of antitrust enforcement. Ever since, US antitrust enforcers have concentrated on businesses’ impact on prices and choice — unlike in Europe, where regulators seek to preserve robust competition.

But some analysts say that the Chicago school approach is outdated in a data-rich internet age which encourages natural monopolies. The consumer welfare standard has facilitated the emergence of companies like Amazon, which use economies of scale and remorseless efficiency to drive down prices, and Google and Facebook, which benefit from “network effects” that promote low-cost expansion.

The rise of the online retailer is an “almost poetic illustration of the shortcomings of current antitrust law”, says Lina Khan, who countered Mr Bork earlier this year in an influential law journal article entitled “Amazon’s Antitrust Paradox”.

The prevailing antitrust approach does not recognise Amazon’s ability to crush competitors by pricing goods below cost and to exploit its power in one sector to gain market share in another, Ms Khan argues.

Amazon has used its heft to extract discounts of up to 70 per cent from delivery companies such as UPS, which in turn makes its own fulfilment service all but irresistible to other retailers, Ms Khan says. Its rivals can “either try to compete with Amazon at a disadvantage or become reliant on a competitor to handle delivery and logistics”, she wrote.

But Amazon’s critics have so far been more persuasive politically than legally, says Diana Moss of the non-profit American Antitrust Institute. “They have not yet articulated a coherent case that would gain traction with enforcers and the courts,” she says. “That’s a heavy lift.”

Politics

Brexit, Trump, Catalonia and the French Election are just a few of the political topics extensively covered by our editorial team. Premium FT.com content helps you to stay ahead of the news as the eventful political landscape experienced in 2017 is still expected to make the headlines this year.

Assuming that prime minister Theresa May does as she says she will and invokes Article 50 of the Lisbon treaty next month, one consequence will be the need for what has been dubbed the “Great Repeal Bill”.

This in itself is something of a misnomer. Far from repealing anything (other than, in due course, the fact of Britain’s EU membership), the statute in question will principally consolidate into UK law a vast array of European legislation, including that which presently exists only as non-statutory rules and judgments.

According to the House of Commons library, some 13 per cent of all primary and secondary legislation between 1993 and 2004 was EU-related. Add to that the rabbit-like explosion of subsequent laws, regulations and rulings, and you start to get some sense of the scale of the task involved.

Making sense of this mountain is one thing, but behind that already daunting task lies an even bigger challenge, which is how to remould the imported “acquis” so it serves the UK economy after the country leaves the EU. That means deciding which laws to change — and then amending or deleting them. It may also mean writing new ones, or creating fresh institutions to fill any voids the country’s exit leaves behind.

To do so will require hard choices about the direction the UK wishes to move in. So far, this is a subject on which the government has been curiously silent, aside from a public promise by Mrs May to leave workers’ protections unaltered, and a somewhat contradictory remark from the chancellor, Philip Hammond, to a German newspaper. In this he indicated the UK might consider changing its whole social and economic model were its negotiations with Brussels not to bear fruit.

Something more strategic is called for. The government needs, for instance, to determine how far it is willing to use this opportunity both potentially to redesign Britain’s regulatory system, and also to reshape the way it bears on the UK economy.

There is certainly a case for decluttering that goes beyond smoothing the bumps and turbulence of exit. Standing still is not really an option. It makes little sense for a Britain that has just recovered its regulatory sovereignty to stick blindly with its inheritance of EU rules and laws.

Then there is the question of the financial burden. While the full cost of national and European regulation can be overstated, it is both large and growing, and was estimated by the Association of European Chambers of Commerce in 2009 to be some 12 per cent of gross domestic product. True, many of these measures may be sensible and their costs proportionate. But that is high compared with the US where the relevant figure is closer to 10 per cent.

And lastly, there are the gains that come from more appropriate regulation. That means re-engineering what are “one-size-fits-all” measures so they fit better with the UK’s national or even geographic circumstances. There are plenty of these to choose from, such as in the financial sector where small domestic lenders or insurance companies are subject to a host of EU legislation that is really designed for larger systemic or cross border companies.

Take also the energy sector, where measures such as the EU’s renewables directive sit on top of the UK’s climate targets. This separately sets out the proportion that must come from specific technologies such as hydro, solar and wind, irrespective of the country’s natural endowments.

In both cases a measure of liberalisation could not only save compliance costs in the short term, but also unleash innovation that would spur longer-term growth.

Seizing these opportunities will take more than simply appending the odd clause to the Great Repeal Bill, or some analogous legislation. It will require the government to find a mechanism for reviewing and amending this great new wodge of laws that commands the confidence of parliament, and to consult with business on which changes to opt for. On top of that, and perhaps more important, Mrs May and her ministers must find the language that persuades an electorate for whom the very concept of deregulation can tend to bring it out in hives.

Britain’s prime minister sometimes gives the impression of wishing to subordinate everything to having a totally free hand in negotiating Britain’s exit from the EU system — as if this was some freestanding task independent of all other considerations. But domestic politics and its imperatives will not stand still during what will be a multiyear process.

Nor will it be easy to know how to play Britain’s hand in Brussels should the country’s leaders not know what they want to happen when exit is achieved.

The Big Read Global politics

Martin Wolf: The long and painful journey to world disorder

As the era of globalisation ends, will protectionism and conflict define the next phase?

It is not true that humanity cannot learn from history. It can and, in the case of the lessons of the dark period between 1914 and 1945, the west did. But it seems to have forgotten those lessons. We are living, once again, in an era of strident nationalism and xenophobia. The hopes of a brave new world of progress, harmony and democracy, raised by the market opening of the 1980s and the collapse of Soviet communism between 1989 and 1991, have turned into ashes.

What lies ahead for the US, creator and guarantor of the postwar liberal order, soon to be governed by a president who repudiates permanent alliances, embraces protectionism and admires despots? What lies ahead for a battered EU, contemplating the rise of “illiberal democracy” in the east, Brexit and the possibility of Marine Le Pen’s election to the French presidency?

What lies ahead now that Vladimir Putin’s irredentist Russia exerts increasing influence on the world and China has announced that Xi Jinping is not first among equals but a “core leader”?

The contemporary global economic and political system originated as a reaction against the disasters of the first half of the 20th century. The latter, in turn, were caused by the unprecedented, but highly uneven, economic progress of the 19th century.

The transformational forces unleashed by industrialisation stimulated class conflict, nationalism and imperialism. Between 1914 and 1918, industrialised warfare and the Bolshevik revolution ensued. The attempted restoration of the pre-first world war liberal order in the 1920s ended with the Great Depression, the triumph of Adolf Hitler and the Japanese militarism of the 1930s. This then created the conditions for the catastrophic slaughter of the second world war, to be followed by the communist revolution in China.

In the aftermath of the second world war, the world was divided between two camps: liberal democracy and communism. The US, the world’s dominant economic power, led the former and the Soviet Union the latter. With US encouragement, the empires controlled by enfeebled European states disintegrated, creating a host of new countries in what was called the “third world”.

Contemplating the ruins of European civilisation and the threat from communist totalitarianism, the US, the world’s most prosperous economy and militarily powerful country, used not only its wealth but also its example of democratic self-government, to create, inspire and underpin a transatlantic west. In so doing, its leaders consciously learnt from the disastrous political and economic mistakes their predecessors made after its entry into the first world war in 1917.

Domestically, the countries of this new west emerged from the second world war with a commitment to full employment and some form of welfare state. Internationally, a new set of institutions — the International Monetary Fund, the World Bank, the General Agreement on Tariffs and Trade (ancestor of today’s World Trade Organisation) and the Organisation for European Economic Co-operation (the instrument of the Marshall Plan, later renamed the Organisation for Economic Co-operation and Development) — oversaw the reconstruction of Europe and promoted global economic development. Nato, the core of the western security system, was founded in 1949. The Treaty of Rome, which established the European Economic Community, forefather of the EU, was signed in 1957.

This creative activity came partly in response to immediate pressures, notably the postwar European economic misery and the threat from Stalin’s Soviet Union. But it also reflected a vision of a more co-operative world.

From euphoria to disappointment

Economically, the postwar era can be divided into two periods: the Keynesian period of European and Japanese economic catch-up and the subsequent period of market-oriented globalisation, which began with Deng Xiaoping’s reforms in China from 1978 and the elections in the UK and US of Margaret Thatcher and Ronald Reagan in 1979 and 1980 respectively.

This latter period was characterised by completion of the Uruguay Round of trade negotiations in 1994, establishment of the WTO in 1995, China’s entry into the WTO in 2001 and the enlargement of the EU, to include former members of the Warsaw Pact, in 2004.

The first economic period ended in the great inflation of the 1970s. The second period ended with the western financial crisis of 2007-09. Between these two periods lay a time of economic turmoil and uncertainty, as is true again now. The main economic threat in the first period of transition was inflation. This time, it has been disinflation.

Geopolitically, the postwar era can also be divided into two periods: the cold war, which ended with the Soviet Union’s fall in 1991, and the post-cold war era. The US fought significant wars in both periods: the Korean (1950-53) and Vietnam (1963-1975) wars during the first, and the two Gulf wars (1990-91 and 2003) during the second. But no war was fought among economically advanced great powers, though that came very close during the Cuban missile crisis of 1962.

The first geopolitical period of the postwar era ended in disappointment for the Soviets and euphoria in the west. Today, it is the west that confronts geopolitical and economic disappointment.

The Middle East is in turmoil. Mass migration has become a threat to European stability. Mr Putin’s Russia is on the march. Mr Xi’s China is increasingly assertive. The west seems impotent.

These geopolitical shifts are, in part, the result of desirable changes, notably the spread of rapid economic development beyond the west, particularly to the Asian giants, China and India. Some are also the result of choices made elsewhere, not least Russia’s decision to reject liberal democracy in favour of nationalism and autocracy as the core of its post-communist identity and China’s to combine a market economy with communist control.

Rising anger

Yet the west also made big mistakes, notably the decision in the aftermath of 9/11 to overthrow Iraqi leader Saddam Hussein and spread democracy in the Middle East at gunpoint. In both the US and UK, the Iraq war is now seen as having illegitimate origins, incompetent management and disastrous outcomes.

Western economies have also been affected, to varying degrees, by slowing growth, rising inequality, high unemployment (especially in southern Europe), falling labour force participation and deindustrialisation. These shifts have had particularly adverse effects on relatively unskilled men. Anger over mass immigration has grown, particularly in parts of the population also adversely affected by other changes.

Some of these shifts were the result of economic changes that were either inevitable or the downside of desirable developments. The threat to unskilled workers posed by technology could not be plausibly halted, nor could the rising competitiveness of emerging economies. Yet, in economic policy, too, big mistakes were made, notably the failure to ensure the gains from economic growth were more widely shared. The financial crisis of 2007-09 and subsequent eurozone crisis were, however, the decisive events.

These had devastating economic effects: a sudden jump in unemployment followed by relatively weak recoveries. The economies of the advanced countries are roughly a sixth smaller today than they would have been if pre-crisis trends had continued.

The response to the crisis also undermined belief in the system’s fairness. While ordinary people lost their jobs or their houses, the government bailed out the financial system. In the US, where the free market is a secular faith, this looked particularly immoral.

Finally, these crises destroyed confidence in the competence and probity of financial, economic and policymaking elites, notably over the management of the financial system and the wisdom of creating the euro.

All this together destroyed the bargain on which complex democracies rest, which held that elites could earn vast sums of money or enjoy great influence and power as long as they delivered the goods. Instead, a long period of poor income growth for most of the population, especially in the US, culminated, to almost everyone’s surprise, in the biggest financial and economic crisis since the 1930s. Now, the shock has given way to fear and rage.

The succession of geopolitical and economic blunders has also undermined western states’ reputation for competence, while raising that of Russia and, still more, China. It has also, with the election of Donald Trump, torn a hole in the threadbare claims of US moral leadership.

We are, in short, at the end of both an economic period — that of western-led globalisation — and a geopolitical one — the post-cold war “unipolar moment” of a US-led global order.

The question is whether what follows will be an unravelling of the post-second world war era into deglobalisation and conflict, as happened in the first half of the 20th century, or a new period in which non-western powers, especially China and India, play a bigger role in sustaining a co-operative global order.

Free trade and prosperity

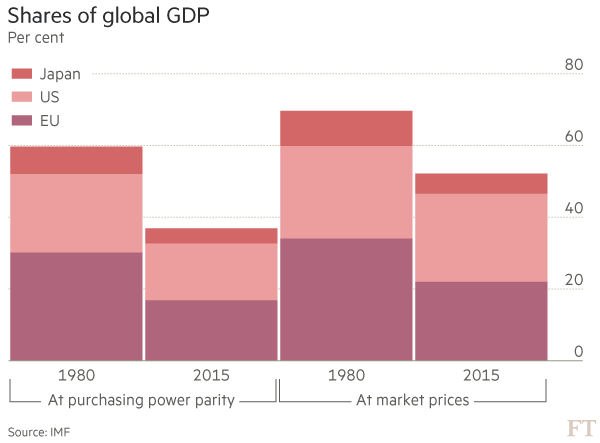

A big part of the answer will be provided by western countries. Even now, after a generation of relative economic decline, the US, the EU and Japan produce just over half of world output measured at market prices and 36 per cent of it measured at purchasing power parity.

They also remain homes to the world’s most important and innovative companies, dominant financial markets, leading institutions of higher education and most influential cultures. The US should also remain the world’s most powerful country, particularly militarily, for decades. But its ability to influence the world is greatly enhanced by its network of alliances, the product of the creative US statecraft during the early postwar era. Yet alliances also need to be maintained.

The essential ingredient in western success must, however, be domestic. Slow growth and ageing populations have put pressure on public spending. With weak growth, particularly of productivity, and structural upheaval in labour markets, politics has taken on zero-sum characteristics: instead of being able to promise more for everybody, it becomes more about taking from some to give to others. The winners in this struggle have been those who are already highly successful. That makes those in the middle and bottom of the income distribution more anxious and so more susceptible to racist and xenophobic demagoguery.

In assessing responses, two factors must be remembered.

First, the post-second world war era of US hegemony has been a huge overall success. Global average real incomes per head rose by 460 per cent between 1950 and 2015. The proportion of the world’s population in extreme poverty has fallen from 72 per cent in 1950 to 10 per cent in 2015.

Globally, life expectancy at birth has risen from 48 years in 1950 to 71 in 2015. The proportion of the world’s people living in democracies has risen from 31 per cent in 1950 to 56 per cent in 2015.

Second, trade has been far from the leading cause of the long-term decline in the proportion of US jobs in manufacturing, though the rise in the trade deficit had a significant effect on employment in manufacturing after 2000. Technologically driven productivity growth has been far more powerful.

Similarly, trade has also not been the main cause of rising inequality: after all, high-income economies have all been buffeted by the big shifts in international competitiveness, but the consequences of those shifts for the distribution of income have varied hugely.

US and western leaders have to find better ways to satisfy their people’s demands. It looks, however, as though the UK still lacks a clear idea of how it is going to function after Brexit, the eurozone remains fragile, and some of the people Mr Trump plans to appoint, as well as Republicans in Congress, seem determined to slash the frayed cords of the US social safety net.

A divided, inward-looking and mismanaged west is likely to become highly destabilising. China might then find greatness thrust upon it. Whether it will be able to rise to a new global role, given its huge domestic challenges, is an open question. It seems quite unlikely.

By succumbing to the lure of false solutions, born of disillusion and rage, the west might even destroy the intellectual and institutional pillars on which the postwar global economic and political order has rested. It is easy to understand those emotions, while rejecting such simplistic responses. The west will not heal itself by ignoring the lessons of its history. But it could well create havoc in the attempt.

Companies & Markets

The Companies section has news and information about the performance of individual companies, their management teams,

shareholders and financial plans. The Markets section delivers breaking stories, insight and data from the global

financial markets.

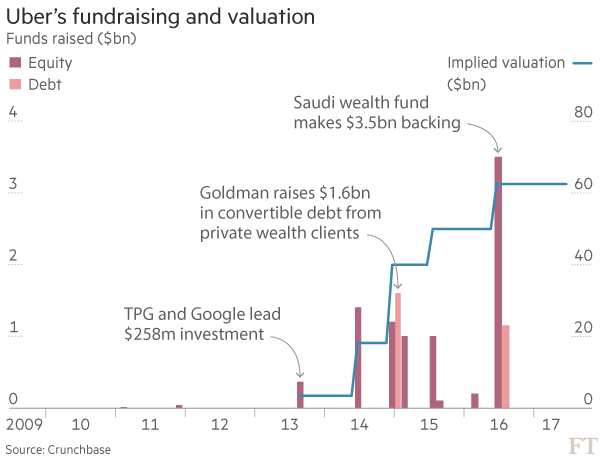

The upheaval at Uber will leave the next chief executive facing an even bigger challenge in how to solve one of the main

conundrums about the company: how does the business of booking a car actually make money.

Uber is the most lossmaking private company in tech history, and the next chief executive will be under pressure to accelerate

the company’s efforts to reduce losses.

During the past four quarters, Uber’s operating losses were more than $3.3bn on a measure that excludes interest, tax and

share-based compensation — a figure that dwarfs other famously lossmaking companies such as Amazon.

The way Uber sees it, booking a car is a commodity product, and the company’s goal is to be the biggest and lowest cost provider

of that product.

To achieve that goal, Uber initially focused on supercharging its markets by injecting huge amounts of capital to attract

drivers and riders. That strategy has been successful in achieving tremendous growth: Uber’s revenues were

$3.4bn in the first quarter of this year, triple the levels of the year prior.

During the past four quarters revenues were $9.1bn, which is more than Twitter or Tesla, and investors valued the company

at $62.5bn last year.

However, the challenge now will be to shift Uber’s model from one that has been very successful at revenue growth, to one

that is more financially sustainable and, eventually, profitable.

Some economists say there was no obvious way to do that, even before the extra challenges Uber now faces as the company rebuilds

its C-suite and tries to recover from a series of crises, including the resignation of Travis Kalanick as

chief executive earlier this week.

“There is no clear pathway I can see for Uber to go from a high-revenue growth company to a profitable company,” says Aswath

Damodaran, a professor of finance at the Stern School of Business. “Normally the story for start-ups is that

as revenues grow economies of scale will kick in, but that story is tough to tell with Uber.”

Furthermore the leadership vacuum at Uber has left a question over one of its main advantages, the ability to raise ample

money at low cost.

Uber has between $6.5bn and $7bn of unrestricted cash in the bank, with a further $2.3bn untapped line of credit. This could

cover the company’s cash needs for roughly three more years, extrapolating from its losses during the first

quarter of this year.

Uber’s path to sustainability will depend on controlling the company’s two main costs: the subsidies for drivers and riders,

and general costs such as engineering and research and development.

These general costs benefit from economies of scale — as Uber grows, the overhead becomes less expensive on a per-ride basis.

The subsidies are essential because Uber uses these as levers to maintain a two-sided transportation marketplace, one that

balances driver demand and passenger supply. Sign-up bonuses attract new drivers and maintain a sufficient

driver pool, while more specific bonuses for certain times and places help steer drivers to places of high

demand.

These incentive payments typically come down on a per-ride basis as a new market matures. However, the tenacity of Uber’s

rivals has meant that the company has not been able to eliminate them altogether.

Even in the US, its biggest and oldest market, Uber was not profitable last year, partly because it had to fight off a fresh

push from its smaller rival Lyft.

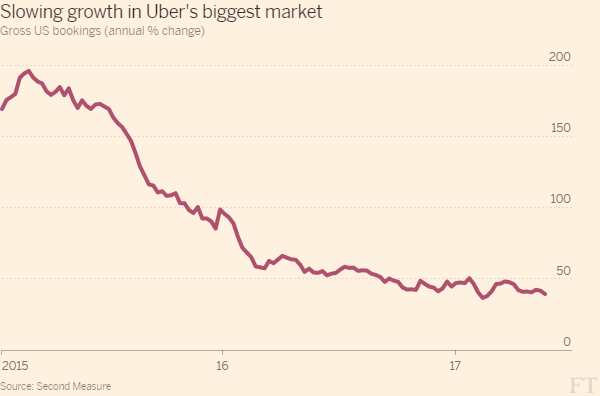

That onslaught has continued this year as Lyft raised fresh funds and benefited from the #DeleteUber campaign: Uber’s market

share has fallen from 84 per cent at the beginning of the year to 77 per cent at the end of May, according

to Second Measure, a research group that analyses credit card data.

The fact that switching costs are so low between one service and the other — both drivers and riders can easily flip between

the apps — means that it can be hard for Uber to defend its market dominance.

Nevertheless the company did succeed in narrowing its global operating losses in the first quarter of this year to $708m,

from $990m the previous quarter.

One area where Uber and Lyft have been experimenting with a different revenue model is through subscriptions — offering a

monthly membership “pack” to frequent riders. (One example might be a $20 monthly fee that buys the rider

20 shared rides for $2 each.)

Subscription models could make sense if — as Uber and Lyft hope — more urban dwellers ditch their private cars and use Uber

and Lyft instead, particularly in cities that lack good public transport.

The fantasy for both companies is that car-booking usage will surge, making private car ownership a thing of the past (right

now ride-hailing accounts for just 0.4 per cent of passenger car miles travelled in the US, so there is still

some way to go).

“Subscription models are always very beneficial,” says Santosh Rao, head of research at Manhattan Venture Partners. “There

is visibility, it is a nice recurring revenue model. To the extent that they can get it, that is great.”

As their markets begin to mature, investors in both companies have come to believe that ride-hailing is not a winner-take-all

market, but rather one in which multiple companies can coexist.

Mitchell Green, an Uber investor and a partner at Lead Edge Capital, says that his thesis is that the ride-hailing market

will keep growing — and both Uber and Lyft will benefit.

He draws an analogy to telecoms companies. “There is absolutely room for multiple players, like AT&T and MCI, there is not

going to be one player in the market.”

This shift has become even more paramount after Mr Kalanick was ousted earlier this week by a group of investors who want

the company to pursue an initial public offering. “The new management means we are probably a little bit

closer to the big IPO than we were before Travis left,” says Rohit Kulkarni, managing director at SharesPost.

As Uber’s new chief executive grapples with the unusual dynamics of the ride-hailing market, they will also have to make

sure Uber lives up to investors’ expectations. With a valuation of $62.5bn, there is a lot riding on the

question of how ride-hailing can make money.

Uber locks horns with homegrown Asian rivals

After an expensive struggle in China that ended in defeat last year to Didi Chuxing, Uber is now embroiled in another costly

strategic battle in south-east Asia,

write Michael Peel in Bangkok and Jeevan Vasagar in Singapore.

The world’s most valuable private technology company is vying with homegrown start-up Grab for dominance of the diverse region

of 10 countries, home to more than 600m people and some of the world’s highest economic growth rates.

The prize is substantial. A joint study by Google and Temasek last year predicted south-east Asia’s ride-hailing market will

grow from revenues of $2.5bn in 2015 to $13.1bn in 2025.

“Exiting China must have been sobering for Uber,” says Adrian Lee, research director at Gartner in Singapore. “South-east

Asia will be critical for Uber to claim true global leadership.”

Singapore-based Grab, founded in 2012, appears to have a solid early-mover advantage. It has expanded aggressively and is

present in 55 cities across a region that arcs from Myanmar to the Philippine archipelago. Uber is in 35

cities.

Grab says it has 2.5m daily rides across south-east Asia, and 70 per cent of the market for private cars and motorbikes —

and it claims an even higher share of the market for taxis summoned by app. Uber declines to give equivalent

information.

Valued at $3bn after raising $750m in a funding round in September led by Japan’s SoftBank, Grab has forged partnerships

with Chinese giant Didi, Uber’s US rival Lyft, and India’s Ola.

Neither Uber nor Grab has turned a profit. But Uber has a brimming war chest: the American company, valued at $62.5bn, had

$7.2bn in cash on hand at the end of the last quarter.

Both have had to improvise repeatedly in south-east Asia to navigate obstacles including sometimes-hostile authorities, severe

congestion and rapidly expanding and changing cities. They also have to serve differing client bases in a

region of vast income variations.

Grab has pushed into mobile payments as it seeks to bind customers closer. The company aims ultimately to be a dominant force

in regional ecommerce for the region, and wants to make more sophisticated use of the large volume of data

it is gathering on customers’ movements and their preferences to offer additional layers of service, according

to Anthony Tan, a Grab co-founder.

Despite Grab’s early claims of primacy, all remains to play for in south-east Asia — and much information about the performance

of both companies is still unclear. But analysts say Uber may face problems if it has already fallen behind

in the race for customers in a market where it is likely to be difficult to change people’s preferences given

the similarities of the apps.