Welcome to the Best of the FT:

Healthcare & Pharmaceuticals

Below you’ll find a curation of the top read articles of our award-winning journalism from 2017 amongst your peers in Healthcare

& Pharmaceuticals. This selection showcases a range of topical news articles, exclusives, popular features

as well as premium commentary and analysis.

We spoke to Trump about Twitter and Juncker about the Brexit bill as well as the people suffering ‘Shit Life Syndrome’

and we investigated the murky world of London’s spies for hire and the ownership of China’s most aggressive deal

maker. Turn to the FT for market-moving exclusives.

When Cary Parton pulled a back muscle playing golf four years ago, he hardly gave it a second thought. But after several

fruitless trips to a chiropractor, a series of X-rays led to a grim discovery: Mr Parton was suffering from

advanced lung cancer that had spread to his bones and organs. The tumour in his liver was the size of a fist.

He was given two rounds of chemotherapy, neither of them successful, at which point doctors told his wife he might be dead

in six months. He was 59.

“The big goal was to see my 60th birthday,” he recalls.

Then, in June 2013, Mr Parton enrolled in a trial at the nearby University of California, Los Angeles, where he received

a new type of drug made by Merck & Co, the US pharmaceuticals group. The medicine, Keytruda, was a checkpoint

inhibitor — a type of immunotherapy that removes brakes in the immune system to unleash the body as a weapon

against cancer.

The drug saved his life. Before starting the treatment, Mr Parton had been virtually crippled by bone tumours that were pressing

on his spine, causing multiple fractures. But by the time he celebrated his 60th in October 2013, he “felt

pretty good”. The following January he returned to work. Today his weekly exercise regime consists of three

trips to the gym, several three-mile walks and a round of golf on Sunday. His tumours have shrunk by 95 per

cent.

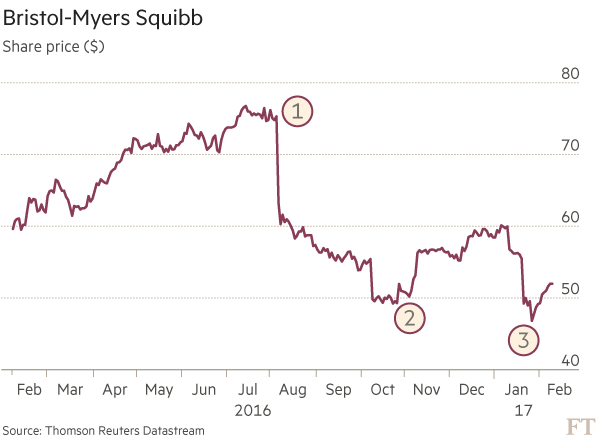

Trial is no tonic for BMS

1. Aug 5 BMS reveals trial of Opdivo had failed against chemotherapy in head to head trial

2. Oct 30 The company publishes full results of clinical trial

3. Jan 20 BMS says it not seek quick approval of its immunotherapy combination

Since the first checkpoint inhibitors went on sale in late 2014, they have produced some remarkable results, helping even

the sickest patients survive for months or years longer than might have been expected. Mr Parton is one of

the lucky ones — despite all the enthusiasm, the drugs only benefit 20-30 per cent of cancer sufferers. “Immunotherapy

is not a silver bullet,” says Bob Hugin, chairman of Celgene, the biotech company. “Checkpoint inhibitors

only work in a minority of patients.”

Early hopes that pharmaceutical companies would be able quickly to raise response rates by combining the drugs with other

medicines have not yet been borne out by large scientific studies. Now the leading makers of immunotherapies

are racing to find a way of extending their benefits to a larger group of patients, while justifying the

lofty valuations bestowed on them.

Pathways to progress

Recent events at Bristol-Myers Squibb, which helped pioneer checkpoint inhibitors, suggest progress will not be smooth. In

August, the company dropped a bombshell when it revealed its checkpoint inhibitor, Opdivo, had flunked a

large clinical trial, which concluded the medicine was less effective for untreated or “first-line” lung

cancer patients than chemotherapy.

Patients taking Opdivo survived on average for four months before their tumours started to grow or spread, whereas those

on chemotherapy — the poisonous cocktail of drugs that has been a mainstay of cancer treatment for decades

— went for six months before their disease progressed. After sailing through every previous trial, most investors

had expected Opdivo to succeed in the study. Mark Schoenebaum, a veteran pharmaceuticals analyst at Evercore

ISI, the investment bank, described the failure as “the biggest clinical surprise of my career”.

Bristol-Myers insisted it could recover by developing a combination medicine that paired Opdivo with Yervoy, an older, complementary

therapy that releases a different brake in the immune system. The company told investors it might be able

to seek rapid regulatory approval to use the combination in first-line lung cancer patients at some point

this year, having been encouraged by the results of earlier scientific studies.

But last month the company upset investors again when it said it had “decided not to pursue an accelerated regulatory pathway”

for the combination therapy following a review of clinical trial data. Its reluctance to share further details

with analysts has left investors speculating as to what prompted such a swift change of heart.

In a statement this week to the Financial Times, Giovanni Caforio, Bristol-Myers’ chief executive, said: “While acknowledging

the competitive landscape continues to evolve, we believe the combination of Opdivo and Yervoy has the potential

to play an important role in first-line lung cancer [treatment].”

Investors have been unnerved too by the actions of AstraZeneca, which is studying a combination of two immunotherapies that

is very similar to the one being investigated by Bristol-Myers. Last month, the Anglo-Swedish drugmaker pushed

back the completion date for its large lung cancer trial and altered the design. Some interpreted the move

as a sign the company was losing faith in the virtues of twinning the two medicines. Shares in Bristol-Myers

have fallen by as much as 30 per cent since August, while its market capitalisation has dropped by more than

$35bn to $87bn over the same period

The industry’s choice

The company’s travails reflect the unpredictability of drug development and the giddy excitement that can take hold on Wall

Street in the early stages of a medical breakthrough. Some analysts were predicting that Bristol-Myers would

generate up to $12bn of revenues from Opdivo by the end of the decade, as oncologists chose its immunotherapies

rather than chemotherapy to treat the majority of lung cancer patients. They proffered such estimates even

though there had been no large clinical trials showing the drug was better than existing treatments for most

patients.

Since launching Opdivo in December 2014, Bristol-Myers has built a blockbuster drugs franchise, generating nearly $3.8bn

in sales last year. It secured regulatory approval to treat melanoma, before winning permission to use the

medicine on a range of other cancers including Hodgkin lymphoma and those in the kidney, and head and neck.

But the main driver of revenues has been the rapid uptake among oncologists treating “second-line” lung cancer that has already

been treated with chemotherapy, but which is no longer responding to the treatment.

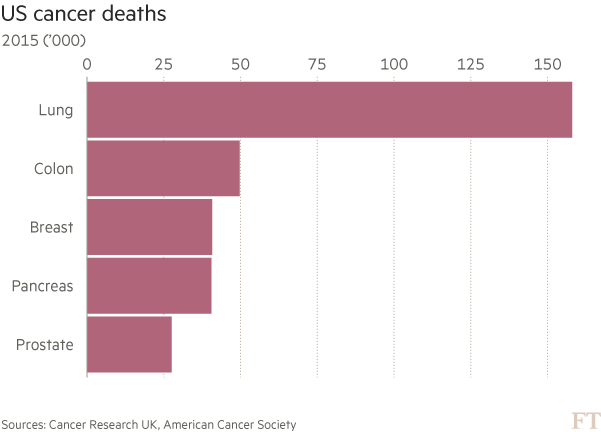

The biggest prize is yet to come: the chance to usurp chemotherapy as the drug of choice for untreated first-line lung cancer

patients, described by analysts at Leerink, an investment bank, as the “single largest market opportunity

in oncology”. The American Cancer Society says about 222,500 people will be diagnosed with lung cancer in

the US this year, while about 156,000 will die from it. Only breast and prostate cancer are more common,

although they kill far fewer people.

Bristol-Myers’ hopes of dominating the first-line lung cancer market started to fade with the failure of the trial in August,

and have dimmed further still since it dashed expectations for a quick approval of its combination therapy.

Now some investors say they detect hubris in the company’s strategy.

When the lung cancer trial failed, the company’s subsequent conviction in the effectiveness of combining Opdivo with Yervoy

gave false hope, say investors.

“Shareholders are angry — a ton of people loaded up on the shares [after the first trial failed],” says Brad Loncar, founder

of the Loncar Cancer Immunotherapy exchange-traded fund, which holds shares in Bristol-Myers. “But in hindsight,

they exuded too much confidence about having a plan to get out of the hole in a semi-near timeframe.”

Another investor says the company has been “ideologically dogmatic” about the benefits of combining two immunotherapy drugs.

Analysts suggest the fall in Bristol-Myers’ value has turned it into a takeover target, most likely for Pfizer or Novartis.

“Why doesn’t Pfizer just buy Bristol-Myers today, given its floundering share price,” asked Timothy Anderson,

an analyst at Bernstein, in a recent note to investors, adding that he expected the drugmaker to bide its

time.

Investment bankers have started to chatter about such a takeover, according to one senior banker, who says Wall Street is

salivating at the huge fees that would be earned by working on a transaction that has the potential to be

the biggest pharma deal of all time.

Analysts say the biggest beneficiary will be Merck. “It is pretty amazing that the company that drove all the innovation

is slowly becoming second fiddle,” says one large life sciences investor who holds shares in both companies.

Whereas Bristol-Myers tested its drug in a broad group of lung cancer sufferers, Merck limited its trials to smaller subsets

of patients that it thought would be most likely to respond. In doing so, Merck limited the size of its commercial

opportunity, but also reduced the chance of flunking a large clinical study.

As a consequence, Merck’s Keytruda has been approved to treat a group of first-line lung cancer patients who have tumours

that contain high amounts of a protein known as PD-L1, which is thought to make them good candidates for

checkpoint inhibitors. Merck could expand further into the first-line market if the US Food and Drug Administration

approves the use of Keytruda in combination with chemotherapy. The surprise submission in January was based

on a study of 123 patients, which showed that the drugs shrank tumours in 55 per cent of patients versus

29 per cent for chemotherapy alone.

Seeking approval

The FDA often gives the nod to drugs based on limited data, especially when the patients who might benefit are very unwell.

Analysts at Leerink believe an approval could help Keytruda generate $3.8bn of sales this year, more than

doubling its 2016 revenues, allowing Merck to narrow Bristol-Myers’ lead.

Roche, the Swiss pharmaceuticals group, is also trialling its checkpoint inhibitor, Tecentriq, in combination with various

types of chemotherapy in more than 2,400 patients and expects to publish data that might lead to an approval

in the second half of this year.

However, it is unlikely that a single combination will provide a one-size-fits-all solution, according to Roger Perlmutter,

Merck’s top scientist. “What we are going to see is that different combinations will be more advantageous

for different patients,” he says. “This is personalised medicine.”

Dr Perlmutter says that, in an 80-year-old patient who was already suffering from other illnesses, “the idea of giving them

a very aggressive chemotherapy regime in combination with Keytruda doesn’t make a lot of sense”, because

of the side effects. “Whereas in a patient who is an otherwise vigorous 45-year-old stricken with malignancy

who has no other medical problems, you’re going to be a lot more aggressive.”

To that end, drug companies are running more than 800 clinical trials of combination drugs that include an immunotherapy,

according to the Cancer Research Institute, testing the medicines alongside older treatments like radiotherapy

as well as newer experimental compounds. It is impossible to predict which will work best, as evidenced by

Bristol-Myers’ travails.

Dr Perlmutter recounts a story from October, when senior scientists from Merck and Bristol-Myers ended up dining a few tables

away from each other at a restaurant in Copenhagen, where they were attending a medical meeting. Merck’s

scientists had just unveiled their successful trial, whereas Bristol-Myers had just published the full details

of its failed Opdivo study.

“I went over to see them, and they were so pleased, so congratulatory,” he recalls. “I hope that when the shoe is on the

other foot — as inevitably it will be — that I will be as gracious as they were.”

Battling lung cancer: how immunotherapy helps tackle the illness

First-line This term covers the first treatment most commonly given for a disease. With advanced

lung cancer it tends to be chemotherapy.

Second-line This treatment is given when first-line therapy either does not work or stops working.

In the case of advanced lung cancer this is usually an immunotherapy.

Types of lung cancer:

Non-small cell lung cancer About 85 per cent of cases are NSCLC. It typically grows and spreads

more slowly than small cell lung cancer.

Small cell lung cancer This makes up 15 per cent of cases. The tumours have cells that are smaller

than in most other forms of cancer.

Stages of NSCLC:

Stage 0 Only a few layers of cancer cells are discovered in a local area. Treatment consists of

surgery to remove the cells. The percentage of patients still alive after five years is 60-80 per cent.

Stage I Cancer is discovered in the lung tissues but has not spread to the lymph nodes. Treatment

typically includes removing part or all of the lung, and sometimes chemotherapy or radiotherapy. Five-year

survival rate: 60-80 per cent.

Stage II Tumours are larger and have begun to spread to lymph nodes but not to distant organs. Treatment

includes surgery, chemotherapy and radiotherapy. Five year survival rate: 20-30 per cent

Stage III Tumours are larger still and may be impossible to remove with surgery, in which case treatment

includes chemotherapy and radiation. Five-year survival rate: 10-23 per cent.

Stage IV About 40 per cent of patients are diagnosed at this stage. It is the most advanced form

of the disease, in which the cancer has spread to other areas of the body. Surgery is not usually recommended.

Chemotherapy is the first-line treatment for patients, followed by a checkpoint inhibitor. Five-year survival

rate: less than 10 per cent.

Source for survival rates: Cancer Treatment Centers of America

Hay Group uses the Financial Times to acquire and retain business clients worldwide"I use the FT to help me develop my thinking on business challenges my clients face…the FT often covers

issues or events that pertain to my key clients. I can either use these articles in a client conversation,

or they prompt me to drop an email or call a client, using the information in the article as a pretext

for contact"

After Maggie Philyaw developed Type 2 diabetes, she found solace not in the medicines of the pharmaceutical industry, but

the technology of Silicon Valley. Two years ago, her then employer in North Carolina signed Ms Philyaw up

to a programme run by Livongo Health, a California-based start-up, which gave her a device, smaller than

an iPhone and fitted with a cellular chip, that keeps track of her blood sugar levels.

Using the latest advances in cloud computing, the drop of blood she draws each day is instantly analysed, and a text telling

her what to do — “drink two glasses of water and walk for 15 minutes” — is sent if her readings place her

in the danger zone. At the press of a button she can also access further help over the telephone from her

“coach”, a highly qualified dietitian who has managed her own diabetes for more than 40 years.

For the titans of big pharma, Ms Philyaw represents omen and opportunity, as a disruptive breed of digital innovator becomes

the access point to healthcare for hundreds of thousands of patients and threatens to undermine the industry’s

decades-old business model. Big pharma has long focused on the lucrative business of drug development, supported

by armies of sales people deployed to persuade physicians to choose its medicines.

But emerging digital technologies are reshaping the landscape. A new generation of companies is using big data, sensors and

artificial intelligence to provide precise real-time monitoring of patients, especially those suffering from

conditions such as diabetes and chronic obstructive pulmonary disease, which are imposing a daunting burden

on overstretched health budgets.

As a result of the products and services these companies are developing, a patient’s primary point of contact with the health

system can sometimes now be a remote monitoring centre, or disembodied voice on the telephone, instead of

a doctor’s office.

“Rather than buying a pill, [insurers or employers] might buy an overall solution for diabetes,” says Tom Main, a partner

in 7wire Ventures, a venture capital fund that led the first round of investment in Livongo. “And that’s

a very different framework for pharma.”

Now retired from her job as a registered nurse, Ms Philyaw pays $50 a month for Livongo’s service and lives free of medication.

She counts her coach Toby Smithson, whom she has never met but who has offered practical and psychological

support, as her most frequent point of contact with the health system.

“I have a good relationship with my physician but I feel I speak with [Ms Smithson] more often,” she says. “Having a coach

has contributed to fewer doctor visits and less money spent that way. I feel that she really cares if I make

it or meet my goals [on diet and exercise]”, she adds.

***

Glen Tullman, chief executive of Livongo, says as recently as three years ago the technology underpinning his company did

not exist. But corporate America, which is a major provider of health insurance, is taking notice. More than

half the companies in the Fortune 100 are working with Livongo and it is eyeing expansion into Europe, Asia

and Canada.

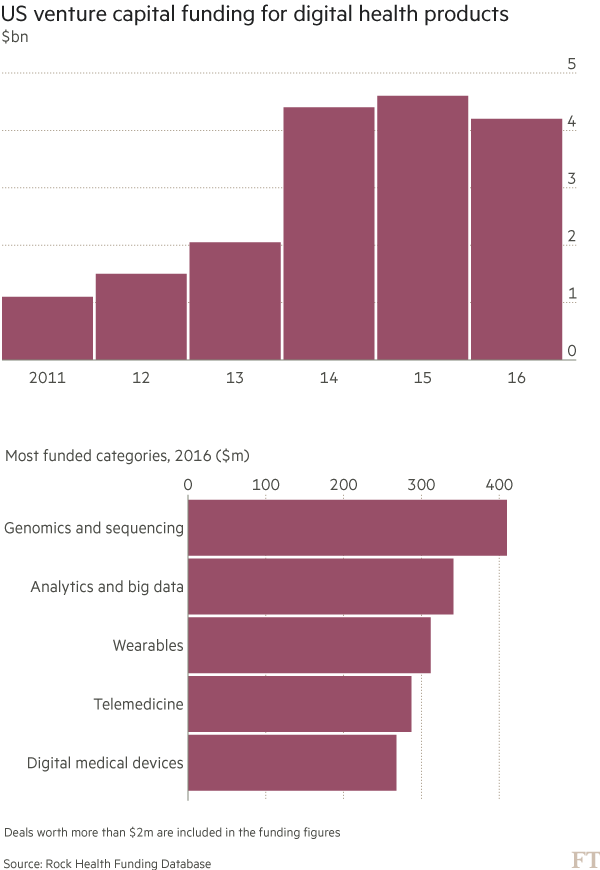

Investors are starting to bet heavily on the potential of technological innovation to transform the way healthcare is delivered.

According to Rock Health, a venture fund dedicated to digital health, a total of $4.2bn was invested in the

sector last year, with companies in the analytics and big data category attracting $341m over 22 deals, more

than doubled from 2015.

However the pharma industry will have to grapple with its own entrenched culture if it is to take advantage of the expansion

in digital technologies.

Stefan Biesdorf, who leads McKinsey’s digital pharma and medical technology work in Europe, says the margins achieved by

a digital health business are small compared with those associated with a blockbuster drug, making it harder

to build a commercial case for investment. Moreover, the never-ending cycle of tweaks and upgrades through

which a digital device passes is foreign to an industry that will wait more than a decade to get a drug from

bench to bedside — but expects to make no further changes once it has secured regulatory approval.

Nor is the industry well placed to exploit a new healthcare universe that requires an ability to build lasting bonds with

consumers. He cites as an example mySugr, a Vienna-based company that uses a similar blend of technology,

combined with on-demand support, to collect data directly from consumers.

“It only has 50 employees but it has much, much, more in-depth understanding of patient behaviour in diabetes than probably

some of the largest diabetes companies, or insulin producers, in the world,” says Mr Biesdorf.

Joe Jimenez, chief executive of Novartis, the Swiss drugmaker that is widely seen as the leader among big pharma companies

on digital health, concedes that the industry has been “slow to adopt some of the digital technologies, compared

to other industries” and recognises “a risk that some of these digital start-ups ‘own’ the relationship with

the physician and the patient and they distance the pharmaceutical company from that”.

However, Mr Jimenez, a former Heinz executive whose background is in the fast moving world of retail, says the industry is

adopting digital technologies “at an accelerated rate”, and argues that they can boast a base of knowledge

the digital minnows cannot rival.

“I do believe that large pharma companies have an advantage, not on the agility side but definitely on what they know about

disease states, about patients, about the entire healthcare system, and many of the start-ups don’t have

that experience,” he says.

Mr Jimenez adds that the digital exemplars are “definitely either potential competitors or they will become partners”.

A flurry of deals in recent years shows that some pharma groups are racing to boost digital capability, by buying companies

that offer ready-made expertise, or entering into partnerships as they seek to offer services “beyond the

pill”.

Teva Pharmaceuticals showed the way in 2015 when it announced it was buying Gecko Health Innovations for an undisclosed sum.

The lure was Gecko’s main product, CareTRx, a platform to help chronic sufferers from respiratory disease,

which combines a sensor device that connects to most inhalers with a data analytics function.

Meanwhile, the French drugmaker Sanofi recently joined forces with Verily Life Sciences to work on devices and patient support

for diabetics, and Pfizer is working with IBM Watson as part of its work on immuno-oncology, using its expertise

in data analytics to identify new drug targets.

Erik Nordkamp, the UK head of Pfizer, says the future of healthcare will involve “a convergence of technologies to come to

better solutions”.

“Both locally and globally we are . . . having discussions with some of these companies to say, ‘what could that future look

like?’,” he says.

***

It is still early days for big pharma’s digital push. Even Novartis, which says it investment in cutting-edge technology

is informing everything it does, has yet to bring any digitally enabled products to the mass market.

One promising programme centres on its heart disease drug Entresto, which has been found to reduce hospitalisation and cardiovascular

death by 20 per cent. It has formed a joint venture with Sanitas, a Swiss health insurer, to offer remote

monitoring and coaching for patients with advanced heart failure.

Yet progress is slow. A pilot project features only 50 patients and will be extended only gradually in the coming months.

Livongo, by comparison, has 35,000 “members”, as it terms its users.

Mr Jimenez points to other Novartis initiatives such as the Breezhaler, a wireless enabled asthma inhaler, and a “smart”

contact lens that can detect blood glucose levels through tears, obviating the need to draw blood, which

will be “much less labour-intensive and much easier to roll out very quickly”.

However, last year trials of the diabetic lens were postponed with no firm replacement date and Novartis is widely thought

to be considering the sale of Alcon, its eyecare unit. (The company says it is “reviewing strategic options

for the Alcon division to maximise shareholder value”.)

The imperative to develop a capability in this field is becoming stronger as health systems demand hard evidence that a drug

is effective and will ease strain on the budget — for example by reducing hospital stays.

Mr Jimenez says the prospect of these new payment structures makes big pharma “quite nervous. They say, ‘if I’m going to

be paid on the outcome of a patient’s health, then I want to be able to control patient adherence, for example,

because if that patient doesn’t take their medicine, then that means I won’t get paid’.”

He estimates that about 25 per cent of all health spending, including on pharmaceuticals, “is not contributing towards a

positive patient outcome”.

Lars Fruergaard Jorgensen, chief executive of Novo Nordisk, the world’s biggest insulin maker, suggests this is the missing

piece for all drugmakers.

“We have spent more than 90 years refining the molecules, yet we have less than 10 per cent of our patients in a level of

control that would eliminate the risk of late-stage complications and that’s not good enough.”

It has teamed up with Glooko, a Silicon Valley company that helps patients manage diabetes, to develop an app that will allow

sufferers continuously to monitor their blood glucose levels. Through another partnership, with IBM Watson,

it will gather data about the impact of its insulin, and patient compliance, that will provide “an increased

comfort level” that it can balance the risks and rewards in future outcomes-based contracts.

Patients who have better knowledge about their health will “also treat [themselves] better, which would lead to higher use

of high quality insulin from Novo Nordisk”, he adds.

One of the biggest problems for the industry, however, is whether an app produced by a pharmaceutical company — and related

to a single branded medicine — would generate the same degree of loyalty from patients and their doctors

as those produced by an independent start-up.

In North Carolina, Ms Philyaw expresses just such reservations. “Personally I probably would prefer a more neutral ground

that wasn’t connected to a drug,” she says.

At Livongo, Mr Tullman is planning to extend its service to cover at least two more conditions by the end of the year.

In a comparison that may resonate in the boardrooms of pharma companies, as they frame their response to the digital revolution,

he likens the impact of these health technologies to that of Uber, which created a whole new market.

“Everybody said it’s going to take the place of the traditional taxi but actually in the US people are using Uber who would

have never used a taxi before.”

He adds: “All of a sudden we can keep people healthier.”

Data ownership: Pharma chiefs formulate response to tech rivals

While some pharmaceutical industry executives remain uncertain how to respond to the digital health revolution, the danger

that tech groups may steal a march by collecting valuable data on their patients serves as a powerful spur

to action.

Andrew Baum, head of global healthcare at Citigroup, says the industry is well aware that companies such as Google, Baiduand

Yahooare investing heavily in artificial intelligence and machine learning to gain insights into patient

behaviour and responses to disease.

“The industry is not quite sure how to engage, because [digital health] is not really their core competence. But on the other

hand, they don’t want someone else to control the data,” he says.

Stefan Biesdorf, a, principal at McKinsey, adds: “In digital health the winners are going to be the companies that sit on

the largest amount of patient-level, granular data . . . a lot of players are taking and building a position

in the market.” IBM, for example, has recently acquired, for several billion dollars, four companies — Truven,

Explorys, Mergeand Phytel— that between them own large amounts of health data.

Some pharma companies are partnering with the major tech groups. Novartisis working with Google Healthon a smart contact

lens.

“The data are key to assessing the patient’s compliance [and] adherence,” says Joe Jimenez, the Swiss drug company’s chief

executive. “Whoever owns that data, or has access to that data, is going to have the power in the system.”

However, the data that exist in a real-world setting, or in health medical records, are stirring “sensitive” issues about

who has ultimate ownership, he says. “Is it the patients, or if the patient waives their right, can a company

own the data itself?”

FT Exclusives Unilever PLC

The $143bn flop: How Warren Buffett and 3G lost Unilever

The story behind the failure of Kraft Heinz to win over the Anglo-Dutch giant

Paul Polman thought it was just going to be an informal catch-up. But it quickly became clear that Alexandre Behring, chairman

of Kraft Heinz, had something very specific on his mind when he visited Unilever’s art deco headquarters

in London last month.

Had Mr Polman, chief executive of Unilever since 2009, ever considered a collaboration with Kraft Heinz, Mr Behring wanted

to know. Mr Polman took this as a sign of interest in Unilever’s spreads unit, home to brands such as Flora

margarine, which his company considered “non-core”.

When he pressed Mr Behring for more details, the Brazilian businessman offered to return soon with a more thorough presentation.

It was clear now to Mr Polman that this was no ordinary visit. He quickly assembled a small group, led by

chief financial officer Graeme Pitkethly, to try to predict what the Kraft Heinz executives might be thinking.

The team began to consider what it viewed as the worst-case scenario: a takeover bid. Even though its US rival was far smaller

than Unilever — a multinational corporation with annual sales of €52.7bn and 168,000 employees — Kraft Heinz

could still afford a debt-fuelled acquisition of the Anglo-Dutch company.

The proposition was one to be taken seriously, given that 50 per cent of Kraft Heinz was owned by two formidable dealmakers,

Warren Buffett and 3G Capital, the secretive private equity group that has been upending consumer industries

from beer to fast food.

Mr Behring, a partner at 3G, returned to Unilever’s headquarters on February 10. Over sandwiches, Mr Behring laid out his

audacious plan: Kraft Heinz would acquire its rival for $143bn, the second-largest takeover in history.

The cash-and-stock offer, which had the full backing of Mr Buffett and 3G’s founder Jorge Paulo Lemann, would create a global

consumer powerhouse. Yet the proposal, to say nothing of the $50-a-share bid, which Mr Polman thought grossly

undervalued his company, was appalling to the Dutch chief executive.

“The idea of being acquired appeared to blow his mind,” one person said about Mr Polman’s reaction to the offer.

Paul Polman: 'The idea of being acquired appeared to blow his mind' says one person about the Unilever CEO's

reaction to the sale

Another insider said: “When they put something on the table, Paul was just utterly categorical that there was

no merit. He gave a number of reasons why there was no interest in such an offer.” The offer was rejected

immediately.

Mr Behring was surprised by Mr Polman’s unequivocal response. He thought their first meeting had gone well. This misreading

would be the first in a series of mistakes that resulted in the bid’s collapse only nine days later.

When Kraft Heinz unexpectedly withdrew its bid on Sunday, it handed the first public defeat to a group of globetrotting investors

who are not used to seeing their ambitions thwarted. The Financial Times interviewed more than a dozen people

involved in the takeover battle to reveal how Unilever was able to beat back their offer.

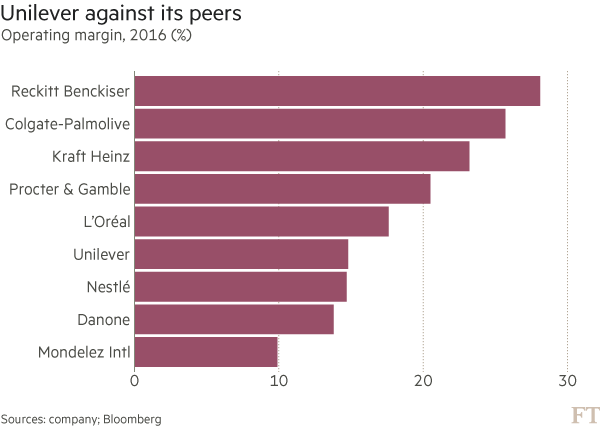

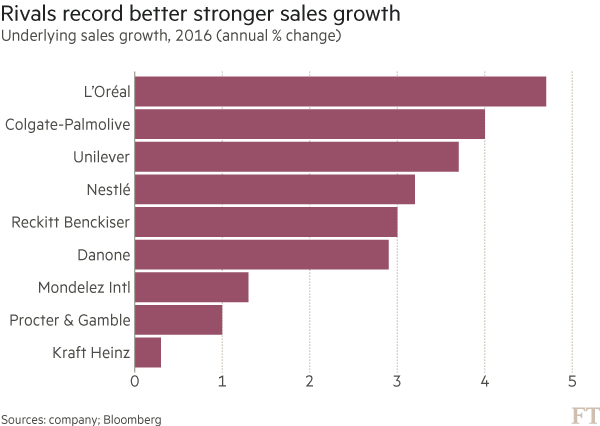

A deal would have created the world’s second-largest consumer company by sales behind Nestlé. For the maker of Kraft Mac

& Cheese and Heinz Tomato Ketchup, it would have more than tripled last year’s annual sales of $26.5bn

and given the predominantly US-based group a deeper reach into emerging markets where Unilever dominates.

Polar opposites

From Mr Behring’s point of view, the timing was ideal. The 17 per cent slump in sterling since the UK voted

to leave the EU in June meant he could buy some of the world’s most recognisable brands — from Dove soap

to Ben & Jerry’s ice cream — in a once-in-a-lifetime sale.

For the Brazilian billionaires behind 3G, a Unilever acquisition would cap nearly 25 years of ever larger deals, including

investments in beverages group Anheuser-Busch InBev and Restaurant Brands International, the owner of Burger

King and Tim Hortons.

“The deal made perfect financial and strategic sense for them, but absolutely none for us,” says one person close to Unilever.

Kraft Heinz had misread Mr Polman, who likes to talk about managing growth for the longer term. By investing in its brands

and promoting initiatives such as environmental sustainability, Mr Polman has sacrificed short-term profits

for longevity.

In contrast, 3G has rapidly transformed the consumer industry by slashing costs, cutting jobs and raising profit margins.

In a sector buffeted by slower growth and changing consumer habits, investors have cheered its austere management

discipline, including a strategy known as zero-based budgeting. Rivals have recoiled at what they view as

a model that ultimately destroys businesses by starving them of investment.

Yet some investors have questioned whether 3G’s tactics are too mercenary. Mr Buffett, who has built up a grandfatherly image

as a hands-off acquirer and advocate of well-run companies, has faced criticism even from his own shareholders

about 3G’s more ruthless approach to dealmaking.

“I tip my hat to what the 3G people have done,” he said in response to a question at Berkshire Hathaway’s 2015 annual meeting.

He added that there were “considerably more people in the job than needed” at companies that 3G had bought.

A combined 13,000 workers have been cut since Mr Buffett and 3G purchased HJ Heinz and merged it with Kraft

Foods in 2015.

Still, 3G’s critics in the industry have been forced to respond to its aggressive management style — including Mr Polman,

who last year outlined a three-year plan to boost profit margins and growth.

But 3G should have realised that Mr Polman would never fully embrace its philosophy. That would mean that Kraft Heinz may

end up having to go hostile if it wanted to buy Unilever — a tactic Mr Buffett has vowed publicly that he

would never use in his deals.

Kraft also miscalculated on another front: the changes sweeping the UK following the Brexit vote. Theresa May’s conservative

government has become hypersensitive to the notion that British companies can be bought for knockdown prices

due to the economic repercussions of the referendum.

A deal that could have also come with ruthless job cuts would encounter further political resistance — giving

Mr Polman and his team another tool in their defence.

'Get them off the pitch early'

Mr Behring left Unilever’s offices with Mr Polman promising to get a full response from his company’s board after their next

meeting, set to be held later this month. Mr Polman immediately called and hired Nick Reid and Robert Pruzan

of Centerview Partners as his financial advisers.

Unilever’s team eventually grew to include Henry Stewart and Mark Rawlinson at Morgan Stanley, UBS, Deutsche Bank, law firm

Linklaters and Tulchan Communications for public relations.

As the group studied the Kraft Heinz bid more closely it came to understand what the US company was attempting to pull off.

The cost savings from combining with Unilever’s packaged foods business alone were enough to justify a

big premium for the whole company, even though the unit was only 40 per cent of its sales. By that logic,

Kraft Heinz would then be getting the rest of Unilever effectively for no premium.

The group studied 3G-backed takeovers and concluded Kraft Heinz would try to seem as friendly as possible and then increase

its bid in increments until there was sufficient pressure from Unilever investors. This was 3G’s modus

operandi. “We didn’t want to get in that situation, so we needed to hit them early. Our best chance was

to get them off the pitch early,” said another person involved in the company’s defence.

They decided that Mr Polman should press ahead with a long-planned trip to Southeast Asia to not raise suspicions.

Because Kraft Heinz’s courtship was so young, secrecy became paramount to the success of its bid. But by last Wednesday,

some investors and journalists had been notified about unusually high options trading in Unilever’s US-listed

shares.

The next day, Kraft Heinz reported lacklustre quarterly results that investors saw as a sign that the company’s cost-cutting

had reached a limit. Shares in the company sank 5.5 per cent.

Meanwhile, the Kraft Heinz board, which includes Mr Buffett, was holding a tense meeting. They feared that news of their

bid was about to spill into the market, said two people briefed on the mood at that gathering. “The goal

was to try to delay the leak as much as possible,” one of the people said.

By mid-morning on Friday, they were proved correct. The FT’s Alphaville blog revealed the details of the Kraft Heinz bid.

Within half an hour, the US company confirmed it had “made a comprehensive proposal to Unilever about combining

the two groups”. It added that the offer had been rejected but suggested that the door was still open.

Unilever slammed the door shut an hour later. In an unusually terse rejection, it said the Kraft Heinz offer “fundamentally

undervalues” the company and that the proposal had “no merit, either financial or strategic”.

Kraft Heinz had expected its first offer to be rejected but was caught off guard by the harsh language Unilever used. “Everyone

thought there was a relationship of mutual respect but clearly they went out strong on the culture stuff . . . making

Kraft Heinz look like the bad guy and Unilever as the angel,” a person close to the US company said.

Kraft Heinz’s advisers at Lazard and law firm Paul Weiss, its top management and 3G executives regrouped later on Friday

to find a new way forward. Additional advisers including PR companies Finsbury and Joele Frank were brought

on. Shares in both companies soared to close the week. The US group was willing to pay substantially more.

However, more fissures appeared. UK politicians started voicing their concerns about another large British-based company

being scooped up on the cheap by a foreign rival. Unilever could have ended up becoming the third major

UK company to be acquired since the Brexit vote after chip designer ARM Holdings and pay-TV broadcaster

Sky.

Under strain ahead of negotiations with the EU, the May government has further pigeonholed itself with its tough talk on

a strong industrial policy that protected British companies and jobs. Shuttling between London and Paris

to deal with the fallout of a proposed Peugeot-Vauxhall deal that could see thousands of jobs shed, Greg

Clark, UK business secretary, spoke with Mr Behring and Sue Garrard, head of communications at Unilever.

Downing Street instructed officials to look at Unilever’s business in the UK and whether a Kraft Heinz bid would raise any

policy issues, including over the future of the company’s British headquarters, its UK listing, jobs, and

research and development.

Back in London on Saturday, as Mr Polman tapped into his network of contacts, he was informed that Finsbury was working with

Kraft Heinz on PR. Within seconds, Mr Polman blasted off an email to Sir Martin Sorrell, the founder and

chief executive of WPP, the advertising company that counts Unilever as one of its most important clients.

Finsbury, which is majority owned by WPP, was removed from the Kraft Heinz side by the end of the day.

'A surgical decision'

On Sunday morning in London, people close to Kraft Heinz said the US company was determined to make a series of concessions,

including taking on Unilever’s name after the merger as well as offering guarantees to maintain R&D

investments and headquarters in the Netherlands, UK and the US.

But Mr Behring, Mr Lemann and Mr Buffett received a letter from Mr Polman outlining his hostility to a deal. They decided

then it would be better to retreat sooner rather than later. “It was a surgical decision,” said a person

close to the trio. “There is little space for emotions in these circumstances.”

Some of the brands owned by the two companies

At 5:31pm a joint statement by Unilever and Kraft Heinz put to rest any hopes of a deal. It said: Kraft Heinz has the utmost

respect for the culture, strategy and leadership of Unilever.

Although it would be foolish to rule out a 3G-inspired comeback of Kraft Heinz for Unilever, the Brazilian management cannot

return for at least six months under UK takeover rules.

The ultimate decision to pull the plug on the effort was made by the two key billionaires backing the transaction — Messrs

Buffett and Lemann, who wanted to avoid a potentially dirty and public takeover battle.

One person close to Unilever said: “From the lunch, Kraft Heinz should have got the impression that they had got it all wrong.”

Another says 3G and its portfolio companies have a clever way of doing business: “Extreme aggression with a smile, so we

gave them extreme rejection with a smile.”

Undeterred by defeat, 3G’s Mr Lemann and his lieutenants are already planning their next move. A $15bn war chest is at their

disposal, ready to hunt the next consumer goods monster.

services for organisations

Fair & flexible pricing

The Financial Times has an open and transparent approach to pricing its group subscriptions. You’re only charged

for users who need frequent access to our content.

Our network of correspondents provides detailed reporting and essential analysis of major events and trends in the

healthcare and pharmaceutical industries.

by:

David Crow and

James Fontanella-Khan in New York

Healthcare companies have announced almost $30bn of acquisitions since the beginning of the year in the sector’s strongest

start for dealmaking in more than a decade, as Big Pharma scrambles to replace ageing blockbusters by paying

top dollar for new medicines.

Executives, lawyers and bankers said the January deals frenzy could be a sign of things to come in 2018, as large US drugmakers

snap up innovative rivals by spending billions of dollars of cash freed up by Donald Trump’s tax overhaul.

Sanofi, the French pharma company, and Celgene, the US biotech group, unveiled two acquisitions on Monday worth more than

$20bn, taking the total value of global healthcare deals announced so far this year to $27bn, according to

figures from Thomson Reuters.

That represented the best start to a year for healthcare dealmaking since at least 2007, Thomson Reuters said.

Both drugmakers offered hefty premiums to seal the deals, with Sanofi paying $11.6bn for US haemophilia specialist Bioverativ

— 63 per cent more than its undisturbed share price.

Celgene agreed to pay $9bn for Juno, a biotech group developing experimental cell therapies for cancer. The price was almost

twice what the Seattle-based company was worth before rumours of a deal prompted a spike in the value of

its stock last week.

So far this year, buyers of healthcare companies have agreed to pay an average premium of 81 per cent, according to data

provider Dealogic — well above the 42 per cent typically paid in 2017.

Their willingness to agree to such lofty prices underscores a perennial problem for Big Pharma: what to do when successful

medicines lose patent protection and revenues evaporate.

Sanofi is trying to offset declining sales of its top-selling insulin, Lantus, which has lost market share following the

introduction of cheaper “biosimilar” versions. Celgene is preparing for the loss of patent protection on

its top cancer medicine, Revlimid, which will face generic competition from 2022 at the latest.

“As Big Pharma is confronted with drugs going off patent and weak research and development pipelines, they have no choice

but to do significant acquisitions despite pushing valuation metrics,” said Frank Aquila, a senior corporate

lawyer at Sullivan & Cromwell.

Large drugmakers have often turned to buying smaller biotech groups to replenish flagging pipelines, but a steady increase

in the value of such companies has prompted some in the industry to warn of a bubble.

Some executives say the sector could continue to overheat as an indirect consequence of President Trump’s tax reforms, which

have enabled large pharmaceutical groups to access billions of dollars of cash that was trapped overseas.

“Given the access to cash that this pool of companies now has, will we see the value of potential targets run up? I do think

that’s a risk,” said Rob Davis, chief financial officer of Merck, in a recent interview with the Financial

Times.

Mr Aquila added: “The new US tax law puts more cash in buyers’ hands and lower rates make more deals accretive. It’s a powerful

combination.”

Baker McKenzie, an international corporate law firm, predicts the tax overhaul will help push the value of global healthcare

deals to $418bn this year, up 50 per cent compared with last year.

GlaxoSmithKline PLC

GSK chief vows to stop ‘drifting off in hobbyland’ with R&D

Emma Walmsley says UK drugmaker will introduce more commercial rigour

The chief executive of GlaxoSmithKline has said the UK drugmaker will stop “drifting off in hobbyland” by producing medicines

with little prospect of billion-dollar sales, as she seeks to reverse years of underperformance in research

and development.

In her first interview since taking the helm in April, Emma Walmsley also disclosed that she will overhaul the company’s

incentive structure in an effort to sharpen accountability. Senior executives will see a higher proportion

of their bonus targets focused on the performance of their own part of the business, rather than the group

overall.

“I want everyone who’s working on the pharma business to be incentivised to win in the pharma business, not incentivised

for some random corporate thing,” she said.

GSK is widely seen as having failed to nurture blockbusters — drugs with $1bn-plus sales — to guard against income lost from

the end of patent protection on Advair, its asthma treatment, which at its peak of £5.27bn annual sales made

up about one-fifth of overall revenues.

Ms Walmsley, who has spent much of the past four months analysing the failings of the R&D division, said the company

had produced a high volume of new launches but that most had not yielded large sales. Late last month she

announced she was scrapping 30 clinical and pre-clinical programmes.

For many of GSK’s long-serving scientists the change of approach was difficult, she acknowledged. “If you’ve been working

on an asset for decades in R&D it’s very hard to decide it isn’t important enough to take forward . . . so

it’s not surprising that people’s human motivation is to keep progressing stuff,” she said.

However, drugs had been allowed to “go through too late and too far” without a rigorous assessment of their commercial potential.

GSK had also been too atomised, she suggested, structured as “an R&D organisation, a commercial organisation, a supply

chain organisation and a bunch of head office people, not with the same strategy”.

She added that Jack Bailey, GSK’s US head of pharmaceuticals, and Luke Miels, who next month takes up the post of global

head of pharma, would be given a far bigger, and earlier, voice in deciding which assets to pursue, based

on their commercial potential. “We need to put the discipline in place,” she said.

Mr Bailey’s expanded role reflects a greater focus on the US, which Ms Walmsley said was “the biggest market and it’s an

innovation-friendly market so it’s important that we play there competitively and we have room for market

share growth . . . definitely in HIV and respiratory”.

Ms Walmsley also implied that the company may have become too risk averse following events three years ago when it was fined

almost £300m after being found guilty of bribery by a Chinese court.

She said: “When you go through some of the things we’ve been through as a company, particularly in 2014 . . . people can

become afraid to make big bets and by definition in our industry you are making big bets on science.

“You should always be afraid of breaches of compliance. That’s unforgivable. But being unafraid of failure is something I

want to bring back because we have to be creative, whether that’s in our brands, in our consumer business

or the invention of new drugs.”

Big Pharma

The FT keeps you up-to-date on the latest news from all the big players in the Healthcare and Pharmaceutical industry.

GlaxoSmithKline is eyeing potential acquisitions from Pfizer in the US and Merck in Germany as the UK drugs group considers

bulking up its consumer division.

Delivering third-quarter results, Emma Walmsley, chief executive, said that, as a world leader in consumer healthcare, GSK

“would look at these assets . . . in terms of their complementarity to our power brand strategy and our geographic

footprint”.

Ms Walmsley also called for as much transparency “as soon as possible” on the UK’s post-Brexit regulatory and immigration

regimes and revealed that GSK was planning to build new drug-testing centres in Europe to ensure supplies

of its medicines are not disrupted.

Pfizer said this month it would sell or spin off its consumer healthcare business, while Merck is also exploring the sale

of its operations in the sector, with a decision by the end of next year.

Ms Walmsley pointed out, however, that Pfizer — whose consumer division has been valued at $14bn — had only announced the

potential divestment last week. It was “extremely early” and the US company had not even confirmed the business

was for sale.

GSK would “stay focused on returns” and M&A in the consumer field “does not change our priorities in terms of capital

allocation”, she added.

The main focus remained on the core pharma business “and R&D within that”, said Ms Walmsley, who in July announced GSK

was scrapping, or partnering on, about 30 drug development programmes as it sharpens its focus on commercial

returns from its drugs portfolio.

Total revenues at the UK’s largest drugmaker increased 11 per cent year on year to £7.8bn in the three months to September

30, in line with analyst forecasts. Growth was boosted by the weak pound, and sales rose 3 per cent at constant

exchange rates — the same as the second quarter.

Pharmaceuticals and consumer healthcare sales increased but sales of vaccines were flat after accounting for exchange rate

movements. The company blamed increasing competitive pressure on some of its diphtheria, tetanus and whooping

cough vaccines.

Adjusted profit before tax rose 7 per cent year on year to £2.3bn, slightly better than consensus forecasts. Adjusted earnings

per share were also slightly above expectations at 32.5p.

Jeffrey Holford of Jefferies, the investment bank, said performance of the pharma division had been weaker than expected

but this had been offset by a stronger-than-predicted performance in consumer.

Ms Walmsley went on to outline “contingency planning” under way for Brexit. Although GSK did not expect Britain’s departure

from the EU to have “a material impact”, it would involve “real costs”, including the construction of new

testing facilities across Europe.

Calling for clarity on an implementation period of at least two years, she suggested that health was as key an issue as security

and defence. “Fundamentally, we are talking about the supply of vital medicines and the security of supply,

both into the UK and back into Europe,” she said.

GSK shares were down almost 2 per cent at 1,485.34p in afternoon trading in London.

by:

Harriet Agnew in Paris and

Javier Espinoza in London

Sanofi, the French pharmaceutical company, says it plans to agree the sale of its European generics business in the third

quarter and expects to return to earnings growth in 2018.

Announcing full-year results for 2017 on Wednesday, Sanofi said it has narrowed the list of buyers for its roughly €2bn European

generics business to a handful of private equity firms and drugmakers.

Private firms that have made it through to the second round of bidding include Advent International, BC Partners, Carlyle

Group and a consortium of Blackstone Group and Nordic Capital, as well as at least one pharma company, according

to people familiar with the process. The interested buyers are performing due diligence. The private equity

groups all declined to comment.

Under pressure to make up for declining revenues from its diabetes franchise, especially in the US, and following several

failed deals, Sanofi in January announced two biotech acquisitions: Bioverativ for $11.6bn and Ablynx for

€3.9bn.

Olivier Brandicourt, Sanofi chief executive, said on Wednesday: “Overall, after a period of significant reshaping since 2015,

we are positioned to drive growth in 2018.”

The drugmaker said it expects underlying earnings per share to rise between 2 per cent and 5 per cent in 2018 at constant

exchange rates, ahead of a 0.4 per cent drop in 2017. It expects foreign exchange moves to have a negative

impact of between 3 and 4 per cent for the year.

Sales rose 4.1 per cent at constant exchange rates in the fourth quarter to €8.7bn, in line with a Reuters poll of analysts.

Revenues at Sanofi’s diabetes and cardiovascular division fell 19 per cent in the period to €1.3bn.

Underlying net income dropped 10.8 per cent at constant exchange rates during the three months to €1.3bn, below Reuters analyst

estimates of €1.46bn.

The group said that it booked an impairment charge of €87m during the quarter, related to its drug Dengvaxia, the world’s

first dengue vaccine and which is at the centre of a health scare in the Philippines. Mr Brandicourt said

Sanofi remained “very committed” to Dengvaxia, adding that “we have absolutely no evidence that the vaccine

has been linked to any deaths”.

Sanofi’s shares shed 2.6 per cent in Wednesday morning trading to sit at €65.80, down 13 per cent on the year.

Private equity bidders for the European generics business are likely to talk up their healthcare experience to convince Sanofi

they are more suitable buyers than corporate bidders, as they come under pressure from their large institutional

investors to invest money, said people with direct knowledge of the process. However these private equity

funds will face steep competition from cash-rich trade buyers that can make a case for synergies easily.

Amgen Inc

Amgen ‘looking hard’ at striking deals using $27bn cash pile

Chief financial officer of world’s largest biotech company cautions on high valuations

Amgen, the world’s largest biotech company, has said it is “looking hard” for deals to deploy its $27bn cash pile but warned

it is struggling to find targets amid soaring valuations in the life sciences sector.

The note of caution comes as mergers and acquisitions activity in the healthcare sector recorded its strongest start to a

year in more than a decade, with almost $32bn of global deals announced since the start of January.

However, buyers have been offering record premiums to clinch deals, with Celgene agreeing to pay $9bn for cell therapy group

Juno — almost twice its undisturbed market value. Sanofi paid a 63 per cent premium for haemophilia specialist

Bioverativ.

“We want to deploy any excess cash and our first priority is to do acquisitions and invest in the business,” said David Meline,

Amgen’s chief financial officer, in an interview with the Financial Times.

But he added: “We see all of these deals announced, and we participate pretty actively in considering whether to bid, but

we haven’t been able to come up with a business case that would make a return for our shareholders.

“We will keep pushing ourselves and keep looking ourselves, because we have lots of financial flexibility.”

He cautioned it would be difficult “as long as people are willing to pay levels above what we deem we can make a return on”.

Mr Meline was talking before the recent market gyrations, which have sent valuations for biotech groups lower.

Amgen’s stance runs counter to predictions of a deals frenzy from bankers and lawyers, who say they are working on more M&A

leads than they have done in years.

The company’s warnings on valuations carry additional weight because it is among the pharmaceutical companies with the most

firepower to do big-ticket acquisitions.

In a recent note to investors, Geoffrey Porges, an analyst at Leerink, estimated that Amgen had as much as $70bn in dry powder

that could be spent on M&A, including $27bn of available cash; the ability to easily raise $40bn on debt

markets; and $3bn in retained free cash flow.

Mr Porges suggested that Amgen would need to do a deal at some point, given that its product sales declined last year, while

the launch of its new cholesterol drug Repatha has fallen short of Wall Street’s expectations.

“Amgen’s growth outlook is not exciting, and the pressure on its legacy products is only going to increase.” said Mr Porges.

He added: “We expect big things, which are most likely to be dilutive to margins and earnings near term, but to confer some

growth and further diversification longer term.”

Inside Business Novartis AG

Novartis faces vexing decisions over asset sales

The disposal of eyecare unit Alcon would be a painful relief

With 123,000 employees, almost $50bn in annual sales and a $200bn-plus market capitalisation, the status of Novartis as a

leading Big Pharma company is beyond doubt.

Yet management, staff and shareholders know that the past five years have been a struggle. Now, critical choices about asset

disposals and investments are looming for the Switzerland-based group.

How it makes them will define the place of Joseph Jimenez, chief executive since 2010, in corporate pharmaceutical history.

Some of Mr Jimenez’s decisions ought to be easier than others. Should Novartis sell its 36.5 per cent share in a consumer

health joint venture with GlaxoSmithKline, the UK drugmaker? Many shareholders think so. Novartis has the

option to compel GSK to buy its stake this coming March. A sale might raise $10bn.

Novartis is undoubtedly examining the ways in which it might put such a tidy sum to use.

Acquisitions to fill holes in its pharma portfolio, or to expand its generics business, would do the trick. If such opportunities

open up, then it will make more sense to sell than to stay hooked up with GSK, even though the joint venture

is doing well and growing in value.

Should Mr Jimenez sell Novartis’s shareholding in Roche, its Swiss rival, potentially raising another $14bn? Again, the answer

is, in principle, yes.

Novartis amassed the stake, amounting to 6 per cent of Roche’s shares but a third of the voting stock, between 2001 and 2003.

The idea was to prepare the ground for a full merger, but that did not happen. These days it is perfectly

clear that it never will.

The most vexing issue is what to do with Alcon, the eyecare division for which Novartis paid Nestlé $51.6bn in 2010.

Like the Roche stake, the Alcon purchase was a throw of the dice for which Mr Jimenez bears no responsibility. Rather, it

is part of the mixed legacy of Daniel Vasella, the former Novartis patriarch who founded the company in 1996

by merging Ciba-Geigy with Sandoz.

When Novartis reported its second-quarter results on July 18, it offered some rare good news about Alcon, predicting that

the division would record a modest increase in full-year 2017 revenue.

Yet Alcon has fallen well short of the high hopes placed on it seven years ago. If Daimler’s acquisition of Chrysler in 1998,

followed by its sale at a vast loss in 2007, was the worst ever deal in the car industry, then Novartis’s

purchase of Alcon is arguably its nearest equivalent in the pharmaceutical sector.

Alcon’s difficulties are by no means the only factor in Novartis’s underperformance, as measured by net sales and operating

profit. Also important are the expiry of the company’s patents for blockbuster drugs and intense price pressures

in the US market.

The financial costs and disruption to Novartis stemming from various legal tangles in Russia and South Korea have not helped,

either.

Still, Alcon is the problem that sticks out. Novartis executives speak bravely about a business that has turned the corner

and, after a few more profitable quarters, will be ready for a sale, spin-off or initial public offering.

However, most estimates of Alcon’s value range from $25bn-$35bn. Even at the top end, that could represent a staggering loss

on the sum Novartis splashed out in 2010.

The Alcon business up for review does not include the ophthalmic pharmaceuticals division that was moved into another part

of the Novartis business in 2016, and which generated around $5bn in annual sales

However, this is less of a concern than what Novartis would do with the money it would receive if it were to dispose of Alcon,

its Roche stake and its share of the GSK-led joint venture.

All told, Mr Jimenez might have $50bn-$60bn to play with. The last thing investors want to see is another Alcon-type purchase

whose value melts like a Swiss glacier.

They can comfort themselves that Mr Jimenez is not Mr Vasella. Novartis has no need for one “transformational transaction”

in the near future, Mr Jimenez says. Carefully targeted, less expensive acquisitions are more likely.

Besides that, investors should keep in mind that Novartis has one of the industry’s finest reputations for scientific research.

As of December 2016, it had more than 200 projects in clinical development. One particularly promising drug, used for treating

leukaemia in children and known as CTL019, is moving closer to the market.

Such breakthroughs require a generous budget. If Novartis sells Alcon or other businesses, it will surely invest some of

the proceeds in research — and investors should welcome that.

What’s next

With Amazon looking to disrupt the industry, what is next for healthcare and pharmaceuticals? The FT provides insights

on what’s next for the industry as a whole.

Every time Amazon enters a sector the stock prices of its listed potential competitors tank. Last year’s purchase of the

upscale Whole Foods sent shares of fellow grocer Kroger and general retailers Walmart and Target down more

than 5 per cent in a single day. Fear of the ecommerce giant is also credited with prompting drugstore chain

CVS to acquire health insurer Aetna in December.

No surprise then that the US healthcare sector sold off sharply after Tuesday’s vaguely worded announcement that Amazon was

teaming up with JPMorgan and Berkshire Hathaway to form a not-for-profit aimed at cutting healthcare bills.

The investor panic is rooted in legitimate fear. Since its 1994 founding, Amazon has seriously disrupted bookselling, general

retail and cloud computing. Along with Netflix, it is reshaping video distribution and is moving hard into

grocery delivery and fashion. Its much-hyped convenience store without checkout lines, which opened last

month, has helped prompt similar experiments by retailers around the world and led to apocalyptic predictions

of the death of millions of retail jobs.

Founder Jeff Bezos sets pulses racing in part because of his demonstrated willingness to invest for the long term, forgoing

immediate profits in favour of building market share. Despite its size, Amazon’s quarterly profits have only

just pushed past the $1bn barrier. Boosted by $789m in US tax reform benefits, it ended up with $1.9bn in

net income on $60.5bn in revenue. By contrast, Apple reported the best quarter in US history, $20.1bn in

net profits on $88.3bn in revenue.

But Amazon is not infallible or invulnerable. Its foray into telecoms was a disaster. The Fire phone was on sale for barely

a year, and led the company to take a $170m writedown before killing off the project in 2015. Similarly,

Amazon Local, its effort to push into the daily deals and coupons business pioneered by Groupon, shut down

in 2015 after barely three years.

Perhaps more on point, Amazon has already taken one unsuccessful run at pushing down consumer healthcare costs with the 1999

purchase of a big stake in drugstore.com. After failing to bring down prices or attract enough business,

Amazon capitulated and sold the ecommerce website to traditional drugstore chain Walgreens in 2011.

As an American, I know from experience that the healthcare sector is ripe for disruption. There has to be a better way than

a system that required phone calls to convince my insurer to pay for my new son’s hospital stay. (Although

it had covered all my prenatal expenses, the insurer initially insisted he was not mine because he did not

share my last name.)

But Amazon has historically done best in categories where it can grab a substantial or dominant share of the market. Driving

out weak competitors and pushing down supplier prices are key parts of its business model.

The healthcare venture, by contrast, is starting very small — JPMorgan, Amazon and Berkshire have only 1m employees combined.

The companies plan to focus on “technology solutions” to lower costs. But the big savings from negotiating

better prices from doctors and pharma groups would require greater scale. Another employers’ consortium covering

7m workers has been trying to do the same thing without clear benefits.

This is one sector where I genuinely hope that Amazon succeeds but I’m not ready to bet the house on it.

Last March, I wrote a column arguing that US employers should be the first in line to argue for healthcare reform. Unlike

their peers in the rest of the developed world, American companies are liable for covering healthcare insurance

costs for two-thirds of the country’s population. Even if the country’s healthcare spending wasn’t double

most of the rest of the rich world’s, with far worse outcomes, this would still be a competitive disadvantage

in a global marketplace in which rivals don’t have to shoulder that burden.

It is exciting, therefore, that three powerhouses of US business — Warren Buffett, Jeff Bezos and Jamie Dimon — are taking

on this issue by launching an organisation, backed by the combined $1.62tn market cap of their own companies,

that aims to deliver “simplified, high-quality and transparent healthcare at a reasonable cost”.

But which part of the Gordian knot of US healthcare will they be able to unravel, what difference will it make and to whom?

The US has a healthcare system that is totally opaque (amazing but true — we commit to paying for services

before we know what they cost), inefficient (markets are hyper-local and relatively low-tech) and bifurcated

— the rich and poor have wildly different levels of care and outcomes. Together, these three issues have

an impact on productivity and growth, not to mention economic volatility for average people. Healthcare emergencies

and the costs that result are the number one reason for personal bankruptcy in the US.

Rising prices mean that health benefits now make up about 20 per cent of total worker compensation (up from 7 per cent in

the 1950s), which is a contributor to wage stagnation. That is, in turn, a key reason economic growth in

the US isn’t higher.

Already corporate conglomerates such as the Healthcare Transformation Alliance, a group of 46 large companies, have tried

to tackle this. But since the US has no single national healthcare market, contracts and discounts must be

negotiated with individual insurance companies, hospitals and providers.

While politicians, including US president Donald Trump, argue that selling insurance across state lines could solve these

problems, the truth is that healthcare in the US is a very local business. The ability to leverage economies

of scale depends on the number of employees that you can sign up to a particular provider. This is a paradigm

better suited to an old model of jobs for life than the 21st-century gig economy. The triumvirate of Messrs

Buffett, Bezos and Dimon may be able to lower costs for their own workers — whether they can do it for others

without structural shifts in the healthcare industry is doubtful.

A bigger pay-off could come if the triumvirate invests in more innovative methods of delivering care. Healthcare is one of

the least digitised industries in the US, according to the McKinsey Global Institute, which makes it an obvious

target for a company such as Amazon (though it must be very careful to safeguard patient data and not use

it for other commercial purposes). There is also low hanging fruit in developing “bundled” payments, in which

a group of services are offered for a fixed price.

Having given birth to two children at a National Health Service hospital in the UK, I was always amazed that I could have

all my needs — from basic check-ups to specialist visits — provided quickly and efficiently in the same place.

Every provider had access to all my medical information digitally. The fact that this still isn’t the case

in America tells you how far the country has to go.

And yet the biggest challenge in the US healthcare system isn’t technical, but existential. Americans have a sense of entitlement

about many things and healthcare tops the list. Most rich countries decided decades ago that it makes economic,

political and moral sense to provide a basic level of care for all citizens, rather than offering everyone

the “option” of the most cutting-edge medical treatments, whatever the cost.

Yet Americans still hold fast to a mythology that “choice” is what makes the system fair. No matter that fewer and fewer

people have any kind of choice at all — particularly now that Obamacare’s individual mandate, which required

everyone to have some form of medical coverage, has been repealed by Mr Trump. Medicare, the US’s version

of the NHS for the elderly, provides a basic safety net, but it also subsidises a variety of costly and questionable

treatments, money that could be better deployed offering more people more basic services. We refuse to have

a real debate about the fact that resource-draining end-of-life care constitutes the largest share of medical

spending.

In short, we prioritise the individual over the collective, in healthcare as in most areas of our society.

It is the American way. But it’s no longer sustainable. Mr Buffett is right that healthcare costs are a “hungry tapeworm”

eating away at our economic growth and prosperity. The best way to fix the situation would be to do what

every other advanced economy has done and move to a nationalised system. But in lieu of this (as of yet)

politically unfeasible solution, I’m glad that some of the smartest business people in the country are agitating

for change.

Apple Inc

Apple pushes forward with healthcare ambitions

Move to set up medical clinics for employees follows similar step by Amazon

Apple is preparing to launch a network of medical clinics for its employees and their families, in what could be a way for

the tech company to test out its broader ambitions in healthcare.

Tim Cook, Apple’s chief executive, recently described the healthcare industry as an area where the company could make a “meaningful

impact” but the iPhone maker has been typically secretive about its plans.

The discovery of a website for an organisation called the AC Wellness Network provides a clear hint that Apple’s ambitions

extend beyond digital health devices such as its Watch.

AC Wellness describes itself as an “independent medical practice dedicated to delivering compassionate, effective healthcare

to the Apple employee population”, launching in spring 2018.

Job advertisements on recruitment sites including Glassdoor describe AC Wellness as a “subsidiary of Apple”, operating in

the Santa Clara area that surrounds the iPhone maker’s Cupertino headquarters.

“AC Wellness Network believes that having trusting, accessible relationships with our patients, enabled by technology, promotes

high-quality care and a unique patient experience,” its website says. “The centres offer a unique concierge-like

healthcare experience for employees and their dependants.”

According to records from the Internet Archive, the domain name acwellness.com was bought, presumably by Apple, sometime

in the second half of last year.

News of AC Wellness was first reported by CNBC. Apple did not immediately respond to a request for further comment on its

plans or the website.

Apple’s apparent move into medical services follows Amazon’s plan to partner with Berkshire Hathaway and JPMorgan Chase to

create a new not-for-profit healthcare company to try to lower healthcare costs for their collective 1m employees.

The trio’s intention to extend the new company’s services to “potentially all Americans” wiped tens of billions

of dollars from the market capitalisation of traditional healthcare companies such as Walgreens Boots Alliance

last month.

While the scope of Apple’s health centre initiative is still unclear, the world’s most valuable company has been making slow

but steady inroads into the health market for several years.

After the launch of Apple Watch in 2014, it has used its HealthKit and ResearchKit software and data platforms to connect

its users’ health information across third-party apps and into clinical research projects.

Apple is working with Stanford University on a study to see if the Watch’s sensors can detect heart abnormalities. With a

forthcoming software update, iPhone owners will be able to download their electronic medical records from

some US hospitals.

At Apple’s annual shareholder meeting this month, Mr Cook was critical of the US healthcare and insurance system, saying

that it “doesn’t always motivate the best innovative products”. Healthcare companies design for reimbursement

rather than patients’ best interests, he said.

“We are in this really great position that we can do what we’ve always done, which is look at it as the user looks at it,”

Mr Cook said. “The more and more time we spend on this, the more and more excited I am that Apple can make

a significant contribution to people’s lives in this area.”

Group Subscriptions

Get straight to what you need with

myFT

Testimonial"Whether I’m meeting clients in Moscow or talking to new companies in Astana, I need to keep up to speed

with what’s going on, locally and globally. FT.com means I can be confident of accessing timely, relevant

and reliable news wherever I am that day”John Edwards, Business Development Manager for Russia and the CIS

Follow topics of interest, without losing the FT view. Save time by scanning all the latest stories in one

place.

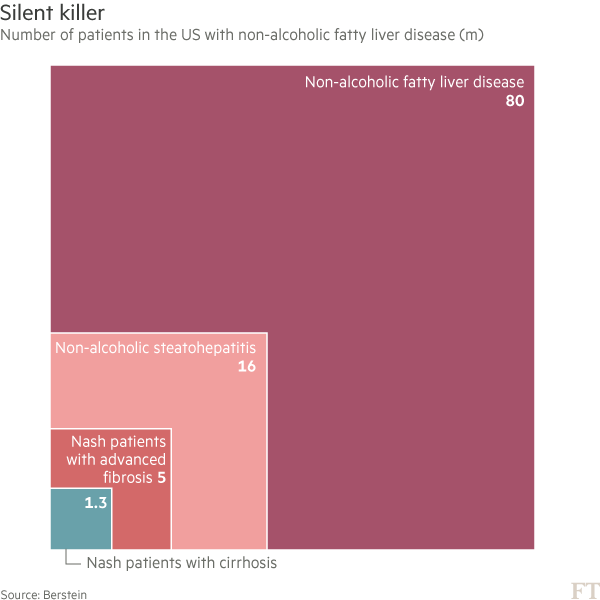

Big pharma thinks it has spotted its next big opportunity — an untreatable silent killer that affects millions of people.

In recent months, large drugmakers including Allergan, Gilead and Novartis have collectively spent billions of dollars acquiring

or licensing medicines designed to treat a liver disease that few people have heard of — non-alcoholic steatohepatitis,

or Nash.

This advanced form of fatty liver disease causes scarring and inflammation of the liver and is thought to affect more than

16m people in the US, according to Bernstein, the investment bank.

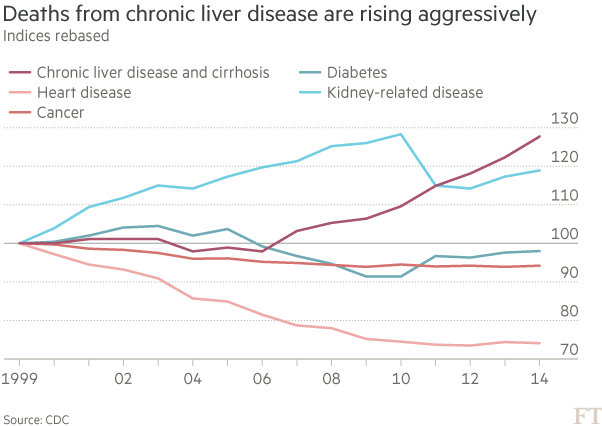

In the most serious cases, the illness causes fatal cirrhosis, while also increasing a person’s chances of developing liver

cancer or heart disease. The US Centers for Disease Control believes there are roughly 20,000 fatalities

each year from chronic liver disease or cirrhosis that are not related to alcoholism.

Drugmakers are betting that the number of people with Nash — which is more common in overweight people — will rise dramatically

in the coming years because of the worldwide obesity epidemic. Some analysts are predicting the global market

for Nash medicines will be worth as much as $35bn a year at its peak.

There are no approved drugs to treat the condition but pharmaceutical groups are studying more than 25 experimental compounds

in humans, with four medicines either being studied in phase III clinical trials, or about to enter this

final stage of testing.

Of the large drugmakers, Allergan is furthest ahead, having spent $1.7bn to acquire Tobira, a San Francisco biotech group,

in November last year. Tobira’s main medicine, Cenicriviroc, will enter phase three trials later this year

with results expected as early as 2019.

Allergan recently acquired another smaller Nash-focused drugmaker, Arkana, for $50m.